By Indexopedia Research Team | October 21, 2024 | In

Most pooled index fund investors are familiar with expense ratios but may not be aware of some of the less obvious costs. Investors need to consider the impacts of other factors such as: internal trading costs, trade spreads, cash drag, lack of quality, phantom taxes, price disadvantages, bond ETF discounts to NAV, and advisor fees (often ranging from 0.5%-1.5%+). Below we’ll discuss how these costs can impact performance and result in less return to the investor.

Expense Ratio

Expense ratios cover costs for a pooled fund’s portfolio management, administrative costs, marketing expenses, legal fees, custodial services, and other operational overhead. Essentially, the expense ratio covers the costs of running the pooled fund and is deducted directly from the fund’s assets. The expense ratio is expressed as a percentage of the net asset value and is available for all public pooled funds.

By purchasing stocks directly, investors can bypass the expense ratios associated with mutual funds and ETFs. This approach allows them to have more control over their investment cost and potentially reduces their overall expenses. With a large investment portfolio, even a slight reduction in expense ratio can result in substantial savings over time.

Internal Trading Costs

Internal trading costs, often referred to as turnover costs, arise from the buying and selling of securities within a pooled fund’s portfolio. These costs include brokerage commissions, bid-ask spreads, and other transaction-related expenses. Mutual funds and ETFs with higher turnover ratios have higher internal trading fees, as more frequent buying and selling of securities leads to increased transaction costs. These fees are indirectly passed on to investors and can erode returns over time.

Interestingly, mutual funds aren’t required to disclose these costs, and when they do, its very challenging to determine what the total cost is on an annual basis. The article by Rob Silverblatt of U.S. News, “How Mutual Fund Trading Costs Hurt Your Bottom Line”, reviews a study by professors from the University of California, the University of Virginia, and Virginia Tech regarding average trading costs for mutual funds. Overall, the internal costs were found to average 1.44%. Large-cap funds’ internal trading costs were determined to be around 0.84% while the costs for small-cap funds measured a substantial 3.17%.

It’s important to recognize that these costs are incurred regardless of what an individual investor in the pooled fund does. The fund will always have to buy and sell securities as new investors enter or leave the fund, or when the index reconstitutes. So even if you pursue a buy-and-hold approach for the fund, you won’t be able to avoid the impact of internal trading costs.

Internal Trade Spreads

Spreads play a role in the overall cost of trading within pooled funds. The spread is the difference between the bid price (the price at which someone is willing to buy a security) and the ask price (the price at which someone is willing to sell a security).

When funds place trades they often have “wider” trade spreads than when an individual is making a trade. This is because the fund itself must buy and sell securities in large blocks. The fund may be selling assets for less than an individual investor would, and buying assets for more than an individual investor would. The result is a drag on the fund’s performance.

Like the other internal trading costs mentioned above, the individual investor incurs these costs regardless of what they do. So even if you’re pursuing a buy-and-hold approach for the fund, you won’t be able to avoid the impact of internal trade spreads.

Cash Drag & Small Investor Herding Impacts

Another symptom of pooled investing is that the actions of the other investors can negatively impact you, regardless of the manager’s skill. As small investors move into and out of the pooled fund every day, it creates more costs as positions are sold to fund redemptions. Oftentimes, this leaves fund managers hostage to small investor behavior, requiring them to maintain a stockpile of cash to fund the redemptions. This cash earns very little return but is still subject to the expense ratio and other pooled investment costs.

Phantom Taxes

Mutual funds must make distributions to shareholders for net taxable realized capital gains within the fund. These capital gains usually result from rebalancing, index reconstitution, or position closure related to share redemptions. Any time securities are sold for a price in excess of their cost-basis, capital gains on the appreciation must be accrued. However, the mutual fund structure often lends itself to even more taxable events when they need to liquidate securities to cover shareholder redemptions.

Mutual funds must make distributions to shareholders for net taxable realized capital gains within the fund. These capital gains usually result from rebalancing, index reconstitution, or position closure related to share redemptions. Any time securities are sold for a price in excess of their cost-basis, capital gains on the appreciation must be accrued. However, the mutual fund structure often lends itself to even more taxable events when they need to liquidate securities to cover shareholder redemptions.

The capital gain taxes assessed in these circumstances are passed along as an expense to existing shareholders, which can force newer shareholders to pay taxes on appreciation they never received. This can be doubly painful when the value of the fund is down overall, but taxes are still due.

Bond Fund Pricing Disadvantages

Mutual funds can buy into bonds that are priced at a premium or discount. This can create pricing disadvantages when investors buy shares of the fund. If the pooled fund holds bonds trading at a premium, investors effectively pay more for the bonds than their face value. Conversely, bonds trading at a discount may lead to lower yields for investors.

Discounts from NAV

Under certain circumstances, funds can trade at a discount to their “net asset value” (NAV). For open-ended funds, this could happen in the case of a sharp market decline; the fund or ETF could be forced to sell illiquid assets at a discount to the estimated NAV. Closed-end-funds trade based on supply and demand throughout the day, meaning they can trade at a discount or premium to NAV. In either case, there is the possibility investors won’t realize the full value of their investment.

Costs from Lack of Quality

Since most index funds select their holdings based on only a few criteria, there is no real consideration for the quality of specific stocks and bonds. Many index funds only include companies based on their market capitalization, or the size of the company. While the company size can provide some information on an investment, it is hardly the type of due diligence needed to ensure quality.

Index funds are passive by nature, designed to mirror the composition of an index. When a stock is delisted from an index, the fund automatically removes it and reallocates the capital into other constituents. This sounds simple enough, but by the time an asset’s value has dropped enough to be delisted, investors in the index funds have already suffered losses. Some notable examples of companies that were delisted include Enron, Lehman Brothers, and AutoNation.

Companies that see their market cap shrink below a certain threshold may be removed to maintain the index’s representation of firms. Despite being a well-known auto retailing brand, a declining market cap relative to peers resulted in AutoNation’s deletion from the S&P 500 in 2017. This removal signaled a rough patch for the company, which faced pressure to evolve in a rapidly changing market environment.

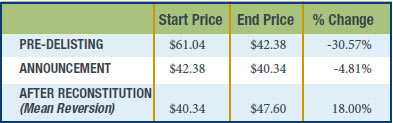

While Enron and Lehman Brothers never recovered, AutoNation did. This highlights another problem with market-cap weighted index funds. AutoNation was removed from the S&P 500 Index in 2017 due to the company’s declining market capitalization and performance relative to other firms in the index. As you can see prior to the reconstitution announcement to be delisted, AutoNation went from $61.04 to $42.38, suffering a loss of 30.57%. From announcement to the end of the grace period the stock further declined from $42.38 to $40.34. After reconstitution and deletion, the stock went up from $40.34 to $47.60. By the summer of 2021 the stock was worth well over $100. Investors would have been better off focusing on quality, rather than just the size of the company.

(Source: Factset)

Advisor Fees

Finally, there is the RIA advisor fee which can range from 0.5% up to 1.5% or more, depending on the advisor. Advisors charge a fee for asset allocation or portfolio construction, but simply invest their clients into mutual funds or ETFs that the advisor has no part in constructing or managing. This effectively means the investor is paying two levels of fees on the same assets; one from the investment advisor for asset allocation, and a second to the product sponsor for actually making the underlying investment decisions.

The Real Costs of Index Funds

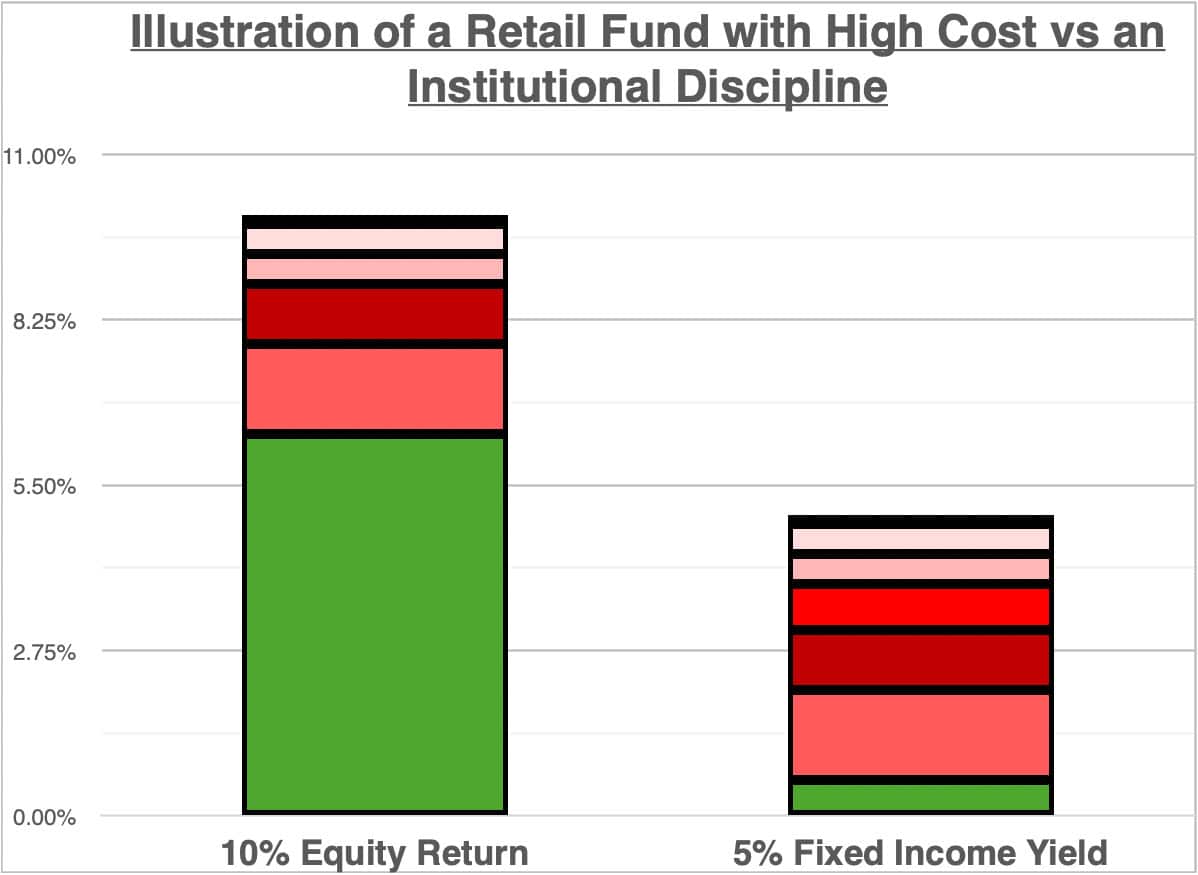

While many clients are aware of RIA advisor fees and expense ratios, they are unfamiliar with the other drawbacks of pooled fund investments. Affluent investors should consider direct-indexing, or indexing using individual stocks and bonds (also known as Institutional Indexing). By owning stocks and bonds directly, investors can screen for quality while avoiding the expense ratios, internal trade costs, internal trade spreads, cash drag, small investor herding impacts, phantom taxes, pricing disadvantages, and discounts from NAV found in pooled investments. The below chart shows how much those costs can add up to reduce overall returns.

*Fees and cost are hypothetical and not reflective of any specific cost associated with a particular fund

Due to the shortcomings of pooled market-cap index funds, many investors prefer earnings-focused direct indexing. Rather than buying pooled products like mutual funds and ETFs, investors can buy individual stocks and/or bonds, thereby circumventing some of the pooled products’ shortcomings. This is why Linden Thomas & Co. built earnings focused institutional indexes by applying earnings quality screens. Direct indexing allows investors to screen for earnings quality. By excluding companies with poor earnings quality, investors can hope to avoid the unhealthy companies included in the index.

Related Articles

What is an Index Fund?

Index Investing,

Top Index FAQs,

Types of Indexes,

October 23, 2023

What Does Your Portfolio and an Onion Have in Common?

Financial Planning,

Personal Finance,

October 1, 2024

Are advisor fees and costs important to investment results?

Investment Principles,

Top Investment Principles FAQs,

January 8, 2025