Even the most well-constructed portfolio will suffer if the investor makes bad choices. It is easy to stay the course when markets are steady, but many investors lose their nerve during periods of volatility or chase returns when they feel they’re missing out. One year of poor or exceptional results can cause uninformed investors to reevaluate their entire strategy. This can be exacerbated by misconceptions about average returns and sector rotation. If your strategy was constructed thoughtfully, with a focus on quality, direct ownership, and spreading risk, then you should think twice before making changes due to recent fluctuations.

Annual Returns

There are generally two types of portfolio returns: annual returns and annualized returns (or average annual returns). Not only are these measured differently, but misunderstandings about them often lure investors into bad investment behaviors which yield weak portfolio results. Let’s first look at annual returns. Annual returns are simply the 12-month result of the investment. If you had invested $1,000 with no contributions and no distributions, the annual returns describe how much your investment would grow in 12 months. Simply put, if your annual return was +8%, your $1,000 earned $80.

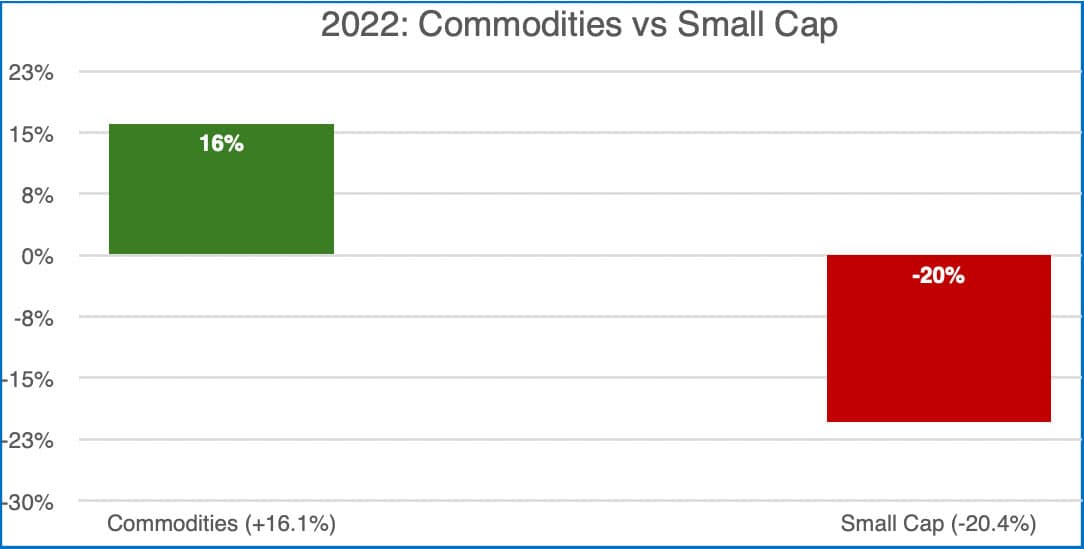

If an investor is looking at annual returns, without an understanding of how different sectors and asset classes rotate in and out of favor, a single year’s good or bad results could convince them to abandon their strategy. Take a look at how commodities and small-cap stocks performed in 2022:

Commodity: Bloomberg Commodity Index, Small cap: Russell 2000

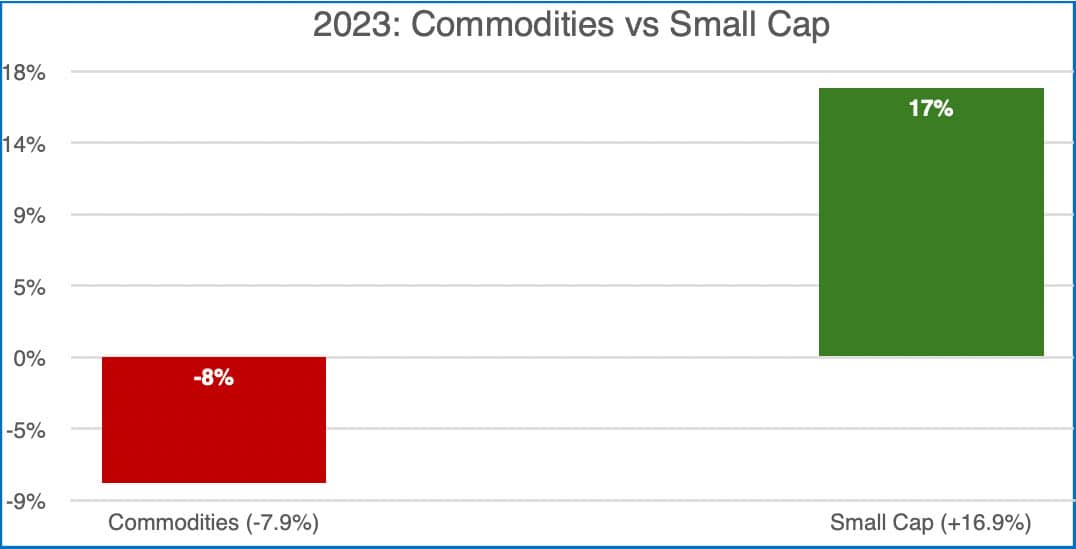

An investor looking at these results might think they should reduce their small-cap stock position in favor of more commodities. If the investor isn’t careful, they could make a big mistake. The next year’s results looked very different:

Commodity: Bloomberg Commodity Index, Small cap: Russell 2000

As you can see from the two above charts, if the investor sold their small-cap positions in favor of commodities in 2023 they would have suffered losses in commodities stocks while missing out on the recovery of small-cap stocks. Instead of buying low and selling high, they are actually selling low and buying high. Short-term results (in this case a single year) could convince an uninformed investor to abandon their long-term strategy. This is why it is important to maintain discipline and not be distracted by every move in the market. Remember, if your portfolio was constructed with direct ownership, diversification, and a focus on earnings quality, patience is the best policy.

Average Annual Returns

While annual returns can be easy to understand, average annual returns are very different. If investors aren’t careful, chasing average annual returns can result in distress and catastrophic results. The calculation of average annual returns represents the constant annual rate of return that would produce the same total growth as the actual fluctuating returns over the investment period. While real returns may vary from year to year, the average annual return smooths out these fluctuations to give a simplified, longer-term view of the investment’s performance.

Because average annual returns are backward looking, the most recent results inflate or deflate the averages and cause investors to chase overvalued sectors and/or leave undervalued ones. While the investor may believe these moves are adding value, this is seldom the case. More likely, they are damaging their results. This is due to a psychological phenomenon called the “recency effect“. People tend to place more importance on recent information, even when they shouldn’t. We typically see this when dominant sectors, such as growth stocks, outperform compared to other sectors, such as value stocks. In that situation, many investors think they should abandon their value stocks in favor growth stocks that are perceived to be the dominant sector.

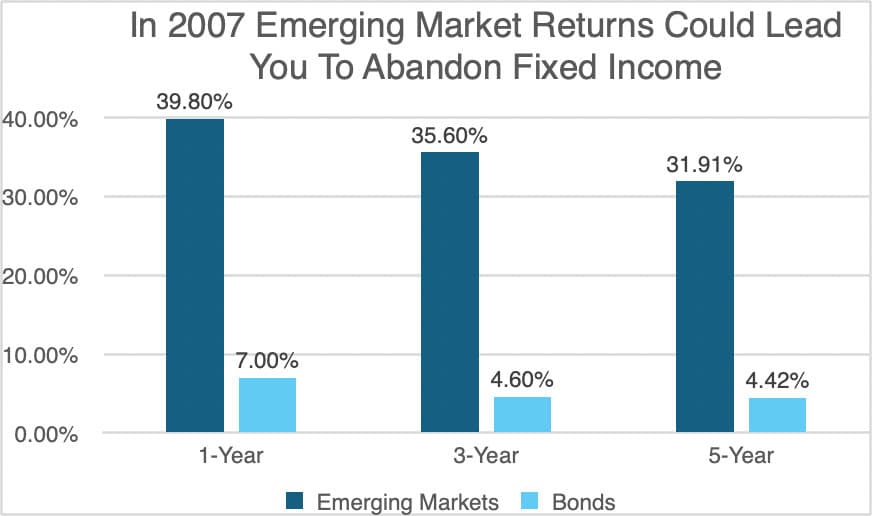

A difference in results for a single year can significantly change the 1-, 3-, and 5-year returns. This often leads investors to seek better opportunities because they are convinced these returns will continue. An uninformed investor may think they will get better results by moving to the perceived greener pastures. For example, take a look at the average returns for emerging markets and fixed income in 2007:

Source: Zephyr

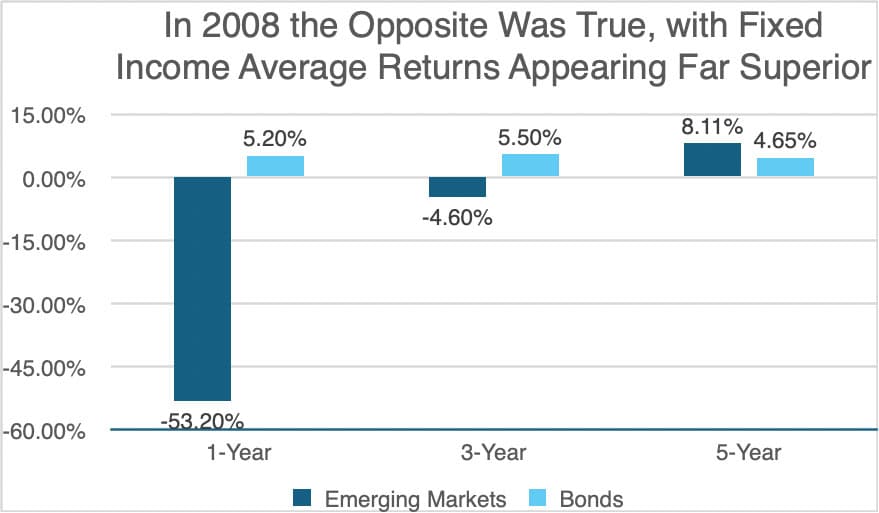

An uninformed investor could see these average returns as proof of emerging market stocks’ dominance over several years and decide to reduce their bond allocation to increase exposure to emerging markets. If the investor built their initial portfolio with a focus on diversification, quality, and direct ownership, they shouldn’t change course just because of recent results. The next year’s average returns could tell a very different story because emerging markets were down significantly:

Source: Zephyr

The investor likely would’ve been better off just sticking to their initial strategy. Once again, if the portfolio is built with a focus on diversification, quality, and direct ownership, they shouldn’t change course just because of recent results. Diversification is important because it is impossible to say for sure what asset classes or sectors will perform well in any given year. By diversifying across sectors and asset classes, and maintaining discipline in their strategy, investors can ensure they are exposed to the dominant asset classes in any given year. Full market cycles can be 10-20 years in length, so even a 7 or 10-year average return won’t tell the whole story.

Below are a few more examples of how drastically average returns can change. Gold had a 5-Year average return of 22.50% in November 2010. Five years later, in December 2015 the average 5-Year return for gold was -6.06%. This doesn’t mean that gold is a particularly unpredictable asset, but it shows how average returns can quickly change.

Source: Zephyr

One of the primary reasons average returns can be misleading is because they are backward looking. In any given year an asset could perform exceptionally well or exceptionally poorly, so it’s important to approach investing with a long-term perspective. Over short time periods, returns are very volatile. Over the long-term, returns can be much more predictable. This is due to a statistical principle called reversion to the mean.

Reversion to the Mean

Imagine a basketball player scores 50 points in his most recent game, even though his average points per game is 30. Would a betting man expect the player to score more than 50 points in the next game? No, because the player is likely to return to his long-term average, rather than his career high. This is an example of reversion to the mean.

Imagine a sector of stocks has a long-term average return of 10%, but last year it returned 20%. Have the fundamental return characteristics for this sector changed? Or was it simply a good year? In the vast majority of cases, it was simply a good year. The characteristics of sectors and asset classes can change over long periods of time, but not overnight. If you build a portfolio for long-term success, you shouldn’t adopt a short-term perspective.

Sector Rotation

With a diversified portfolio, you’ll never have the absolute best performance in any given year. Even when one sector falls out of favor while another dominates, history shows that having money in various sectors and asset classes improves your chances of doing well over time. Over time, sectors and asset classes rotate into and out of favor. Next year the weak sector may become dominant, or vice versa.

The below chart shows how one year’s winner can be next year’s loser:

Source: Bloomberg, FactSet, MSCI, NAREIT, Russell, Standard & Poor’s, J.P. Morgan Asset Management.

Large cap: S&P 500, Small cap: Russell 2000, EM Equity: MSCI EME, DM Equity: MSCI EAFE, Commodity: Bloomberg Commodity Index, High Yield: Bloomberg Global HY Index, Fixed Income: Bloomberg US Aggregate, REITs: NAREIT Equity REIT Index, Cash: Bloomberg 1-3m Treasury. The “Asset Allocation” portfolio assumes the following weights: 25% in the S&P 500, 10% in the Russell 2000, 15% in the MSCI EAFE, 5% in the MSCI EME, 25% in the Bloomberg US Aggregate, 5% in the Bloomberg 1-3m Treasury, 5% in the Bloomberg Global High Yield Index, 5% in the Bloomberg Commodity Index and 5% in the NAREIT Equity REIT Index. Balanced portfolio assumes annual rebalancing. Annualized (Ann.) return and volatility (Vol.) represents period from 12/31/2008 to 12/31/2023. Please see disclosure page at end for index definitions. All data represents total return for stated period. The “Asset Allocation” portfolio is for illustrative purposes only. Past performance is not indicative of future returns.

Guide to the Markets – U.S. Data are as of September 30, 2024.

Over the entire period shown above, large-cap stocks outperformed other sectors and asset classes (see far left column). In 2022 large-cap stocks had a -18.1% return. If that bad year convinced you to reduce your large-cap position, you would’ve missed out on the recovery in 2023 and 2024. You can see similar situations with emerging markets in 2017-2018 (from best to worst), and developed markets from 2016-2018. The point is that no one knows which asset class or sector will perform the best in any given year, so instead of relentlessly chasing the current hot asset, it’s important to maintain discipline and diversification.

The white squares with the line running through them show how a diversified portfolio would perform over this time period. While it was never the absolute best performer, it was also never the worst. The best long-term compounding isn’t found by seeking the top asset class; it’s often found in the middle. When owning a small portion of most (if not all) asset classes, you don’t need to worry about which asset class or sector performs the best at any given time.

The media can also play a role in misleading investors. After the rally of REITs in 2021, it seemed like every infomercial was telling you that you’re missing out on great returns. Of course, real estate can be an attractive investment, but you should not chase last year’s returns.

Time, not Timing

Building a diversified portfolio with direct ownership and quality holdings that’s tailored to your needs requires careful attention and time, but means you never need to chase last year’s hot sector – you already own companies of the highest quality in that sector. When you own both strong and weak performing assets, down-markets present an opportunity to add to the weak positions at a discount. In the 2022 down-market for bonds, investors who added to their bond positions during the dip built principal, increased net income, and enhanced long-term compounding.

Owning companies with high earnings standards in each sector allows investors to fully participate when lagging sectors recover. You are participating in the recovery from valley to peak. Spreading risk between sectors means never having to chase results because you likely already have money in both the dominant and weak sectors. The first inclination of most investors is to invest in top performing sectors, without realizing that it only takes a short 6 or 12-month period for an asset class or sector to go from best to worst, or vice versa. This is why patience and discipline are a principle of Linden Thomas & Co.’s investment philosophy:

Principles of Portfolio Efficiency

- Spread risk across bonds, growth, value, and dividend stocks, and small, mid, and large cap stocks.

- Buy healthy companies that meet high-quality earnings standards.

- Own the companies directly for control and transparency.

- Be patient and don’t chase results.

Once you’ve implemented these four steps, remember: it’s not about timing the market, it’s about time in the market!

Successful investors focus on earnings quality, high net fixed income cash-flow, direct ownership, and spreading risk. There will always be plenty of hype around investment products, whether they are annuities with the promise of high returns, or “get-rich-quick” type investments such as crypto-currencies, dot-coms, etc. The savvy investor knows that their long-term strategy shouldn’t be abandoned due to short-term volatility. An investor chasing returns based on recent results will miss out on the rallies and recoveries that generate long-term wealth.

Related Articles

Historical examples of hot sectors that didn’t end well

History of Markets,

Investment Principles,

Knowledge & Insights,

Markets,

Top Investor Mistakes,

July 11, 2024

Rose Colored Glasses: Why Investing During the Good Times Can Create Poor Allocation Tilts

Investment Principles,

Top Investor Mistakes,

March 6, 2025

The Media’s Role in Fueling Market Hysteria: Lessons for the Prudent Investor

Behavior,

History of Markets,

Investment Principles,

Markets,

September 19, 2024