How Huge Companies are Distorting Sound Risk Management

Over the past decade or more, Large Cap Technology stocks have had quite the run, generating extraordinary long-term returns. From 2011 to May of 2026, a period of about 15 years, the technology sector generated compound average growth rates of about 20% per year, which is significantly better than all other sectors during that time frame. So strong were the leading Tech stocks performance numbers, in fact, they have earned the attention and admiration of investors globally. Consequently, these companies are often lumped into a group with nicknames like the Magnificent 7, the AI Seven, FAANG, and even FAANGMAN, among others. These companies are household names like Nvidia, Google, Apple, Amazon, Microsoft, Facebook (now Meta), Netflix, and Tesla and their extraordinary growth rates have powered the entire market higher.

However, their extraordinary success has made them enormous. And their sheer size has changed the investment landscape. One of the most important milestones of the past decade or so was the day that Apple, Inc (AAPL) – the famed computer and device manufacturer – first eclipsed the $1 trillion market cap level on August 2, 2018. Never before had a publicly-traded company grown so large. Since then, several other technology companies have also surpassed that threshold as well, as noted in the image below:

Source: Linden Thomas & Company

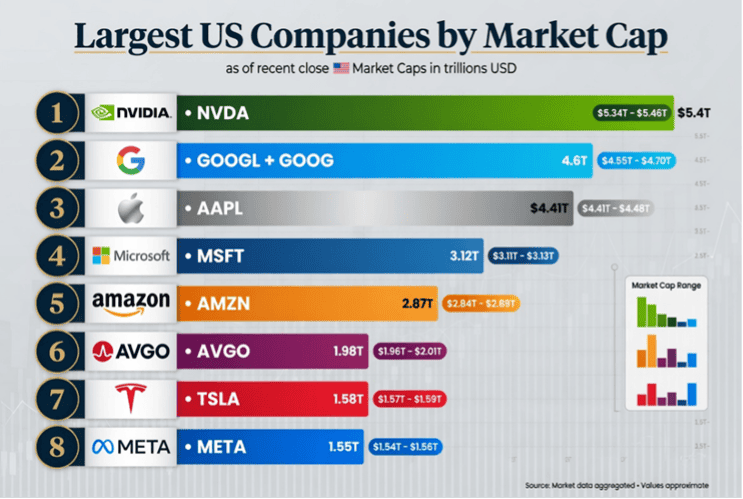

All that is fine and good, however, these trillion-dollar companies are now dominating the standard indexes many investors use to construct portfolios and benchmarks. As you can see from the exhibit above, these behemoths are all in the Technology Sector. And as you can see from the exhibit below, these companies have sailed right past the $1 trillion threshold, and now sport market capitalizations measured in several trillions.

Source: Linden Thomas & Company

At the top of the list sits Nvidia Corp. (NVDA) – the famous AI and gaming chip maker – is now trading at a staggering $5.4 trillion in market capitalization, which also means it comprises between 12% and 14% of major Growth indexes, like the Russell 1000 Growth and the S&P 500 Growth Index. Similarly, Google is not far behind with a $4.6 trillion market cap with combined weights of 8% and 12% in the Russell 1000 Growth and the S&P 500 Growth Index, respectively. And so on from there.

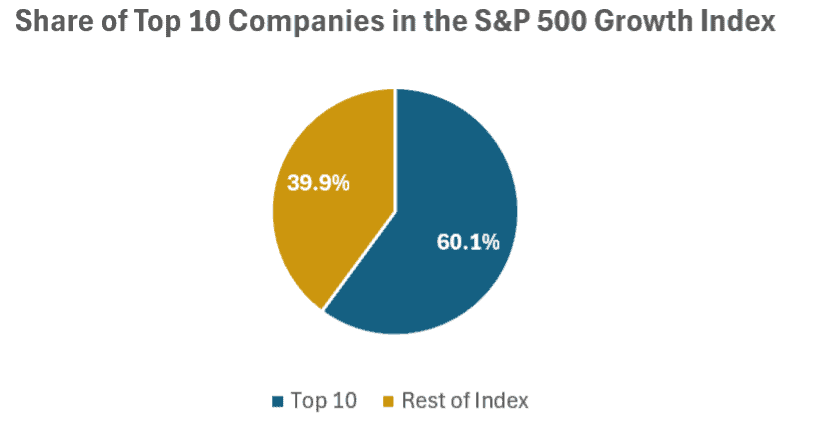

The top 10 largest companies combined now comprise roughly 60% of the S&P 500 Growth Index. These companies have grown so big, the tail is now wagging the dog. While indexes are typically constructed to represent economic activity across the economy, most of them, nevertheless, are market cap weighted. This means that the stocks that do the best get the largest weights.

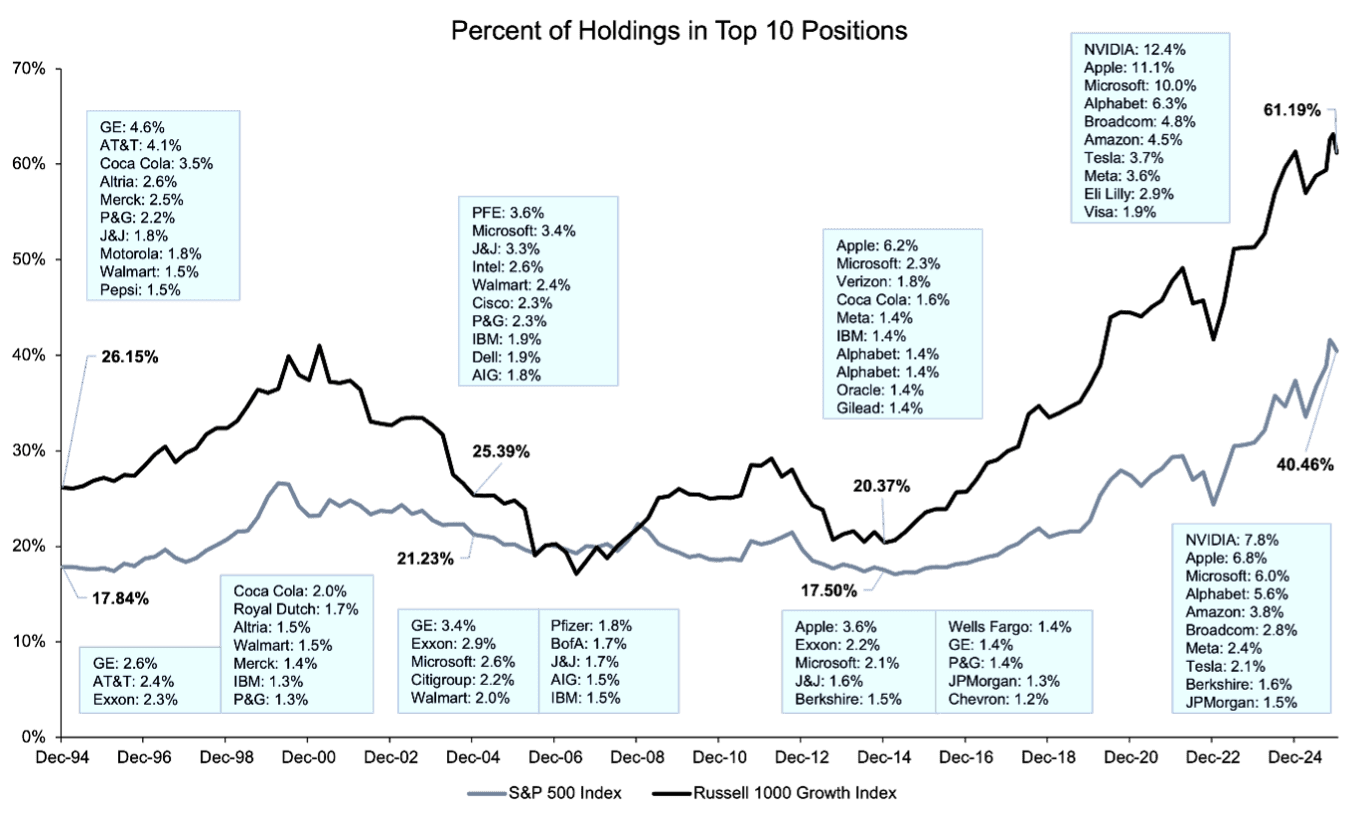

It hasn’t always been this way. Technology stocks have grown so much they have gobbled up a larger and larger share of the indexes over time. For instance, back in 1994, the weight of the top 10 stocks in the Russell 1000 Growth Index was just 24%. That used to be normal. Even during the height of the Tech Bubble of 1999, the weight of the top 10 was only 27%, which looks tame by comparison today. After the financial crisis of 2008, it retreated all the way back to 20.4%. However, from 2015 forward, it has done nothing but go up. Note the dramatic increase in the weight of the top ten holdings from 2015 to today, now comprising over 61% of the Rusell 1000 Growth Index!

As Markets Concentrate Risk, You Should Spread Risk

Markets are mechanisms that enable people to buy and sell securities as they see fit. As such, they are an expression of the hopes, dreams, fears, greed, choices and policies of all the participants. They can be ruthlessly efficient and spectacularly manic; and vacillate between the two over time. But there is no reason ever to believe that you should simply follow the crowd. While the opportunities for businesses operating in the technology sector in general, and AI in particular, may be spectacular, there is an important difference between the business opportunity for the company and the financial returns earned by market participants. Concentrating your wealth in just a small handful of names can be a recipe for disaster if one or more of these monsters disappoint.

Despite the dramatic success these stocks have earned over the past 10 years, a change of fortune to some degree is inevitable. Moreover, you shouldn’t be surprised by it. Everything in the markets moves in cycles. These large tech companies have clearly experienced a long and successful upside in this cycle. Consequently, we should also expect a material reversal at some point. Owning a piece of these companies has indeed been prudent over the past several years. Unfortunately, all too often investors’ focus is looking in the rear a view mirror wishing they had more after a long rally and abandoning balance in the pursuit of chasing something that may have run its course. Owning large companies is good if done using a balanced approach, but chasing them can end in failure, or worse, devastation.

So, being smart about the full market cycle is important. Therefore, develop a sound financial plan that balances your portfolio’s need for growth with your prudence by spreading your risk. Sadly, many simply follow the herd. But their timing, mindset, temperament and emotions are going to be different from yours. So, don’t chase technology stocks simply because they have had a strong run. And definitely don’t get swept up in what the crowd is doing. If you spread your risk and acknowledge the full market cycle, you have a greater opportunity to live to fight another day. When that day comes, you can do better on the downside, have a shorter time to recover, and start compounding money more quickly during the recovery. This discipline helps produce satisfactory returns.

Related Articles

4 Critical Impacts of an Inefficient Portfolio

Investment Principles,

Portfolio Considerations,

January 8, 2025

The Power of Diversification: How Different Asset Classes Complement Each Other in a Balanced Portfolio

Behavior,

Index Sectors,

Investment Principles,

Markets,

Portfolio Considerations,

September 17, 2024

Building a portfolio with a correction in mind vs timing the correction

Investment Principles,

Markets,

Portfolio Considerations,

October 1, 2024