Few events in the markets generate as much excitement as an initial public offering. The headlines promise the next great company, the financial media counts down to the opening bell, and the stock often “pops” the moment it begins trading. The magnetic pull on investors is powerful — nobody wants to miss the next Amazon or the next Apple. But excitement and opportunity are not the same thing.

One of the most consistent messages we share with readers is to stay disciplined and avoid chasing. IPOs are one of the clearest places where that discipline gets tested. To be clear, this is not an argument that you should never own a newly public company. It is a reminder that an IPO is engineered to maximize hype — and that even a wonderful business can be a poor investment if you pay the hype price.

Who Is the IPO Really Designed to Serve?

It helps to start with what an IPO actually is. A company that wants to raise money hires an investment bank — the underwriter — to bring its shares to market. That same bank is responsible for setting the offering price and deciding who gets to buy at it. From the bank’s seat, a “successful” debut is one that is heavily oversubscribed and jumps on the first day of trading. That first-day jump is the dramatic number you see in the headlines.

Here is the part that rarely makes the headline: that pop is not a gift to the public. It is a transfer. Shares sold at the offering price go largely to the bank’s favored institutional clients, and the pop is the reward they capture when the stock opens higher. The everyday investor watching the excitement on television almost never buys at the offer price. They buy at the open — after the pop. So the very return that creates the hype is the return the public rarely gets to keep.

This is not a small effect. Across more than 9,000 U.S. offerings from 1980 through 2025, the average first-day return — the pop — was roughly 19%, and that companies and their early backers left an estimated $250 billion “on the table” in the process. In hot markets the pops run far larger still — averaging more than 40% in 2020 and over 30% in both 2021 and 2025. A first-day jump that large is a signal that the deal was priced to manufacture excitement, not a signal that value is waiting for you at the open.

Source: Jay R. Ritter, University of Florida — Initial Public Offerings: Updated Statistics.

The First-Day Pop Is Not Your Return

By the time you can buy, the story has already been told. The roadshow has made its rounds, the deal is oversubscribed, the narrative is polished, and the price reflects the most optimistic version of the company’s future. Buying an IPO on its first day is a bit like arriving at an auction after the bidding war is already underway. The most enthusiastic buyers in the room have set the price, and you are being asked to match them — on a company with no public track record to check that enthusiasm against.

When the Hype Meets Reality

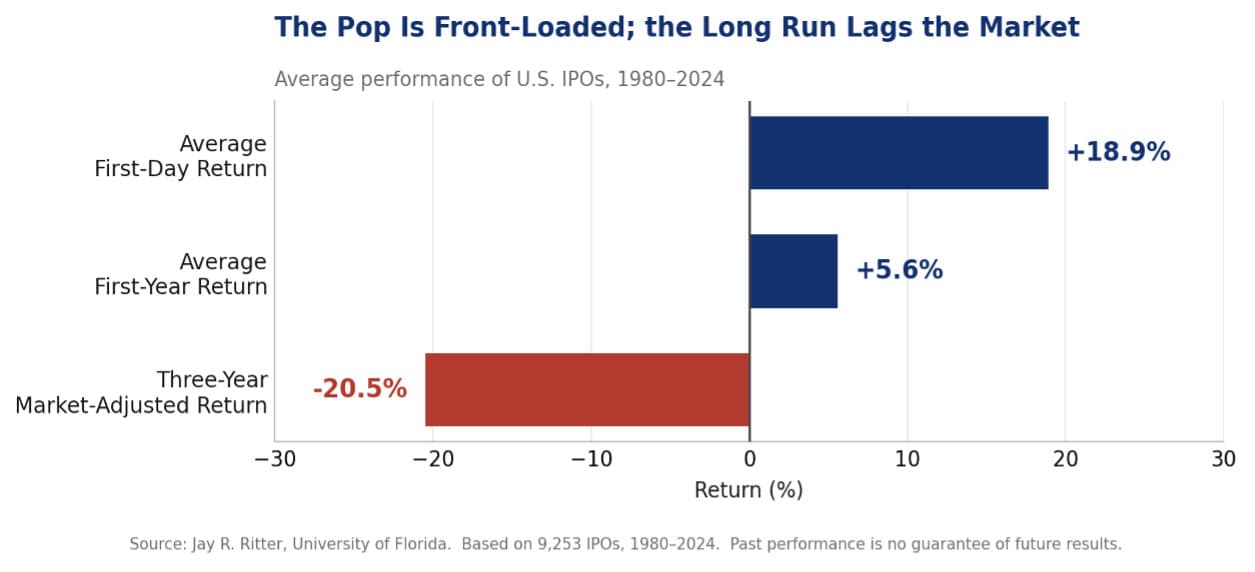

Pull back from any single headline and look at the whole market. Across more than 9,000 U.S. IPOs since 1980, the pattern is remarkably consistent. The chart below follows the average IPO through three moments in its life: its first day of trading, its first full year, and its standing against the broader market three years on.

Source: Jay R. Ritter, University of Florida. Average across 9,253 IPOs, 1980–2024. Past performance is no guarantee of future results

The story is in the order of those bars. The average IPO jumped 18.9% on its first day — the pop. But as we have seen, that gain is captured at the offering price, before the public can buy. From there the excitement fades fast. The average first-year return was just 5.6%, and measured against the market over three years, the average IPO underperformed by 20.5%. The reward is front-loaded into a single day most investors never touch — and what remains has, on average, trailed the market.

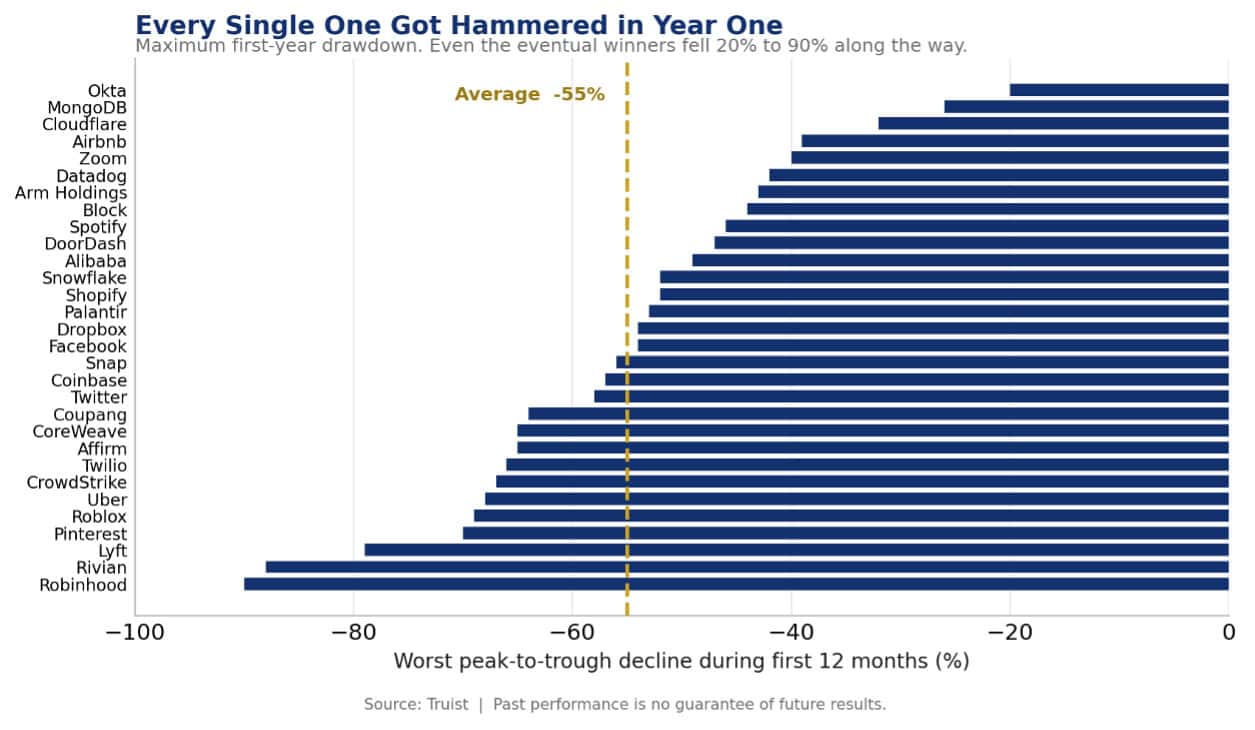

Perhaps the aggregate hides a handful of standout winners worth chasing. So narrow the lens to thirty of the most celebrated technology IPOs of the past decade — household names that arrived with enormous fanfare — measured from their offering over their first year. Two patterns survive even among the famous.

First, only 43% of these names were positive a year after their debut, and the median return was -9%, even though the average was +14%. As we have written before, averages can lie: a few enormous winners — a Palantir, a Zoom, an Arm — pull the average up and quietly mask the fact that the typical name disappointed. If you owned the average IPO, you did not earn the average return; you earned the median.

Second, and most important for discipline, the ride was brutal across the board. The average maximum drawdown in the first year was -55%. Every single name on the list — including the eventual winners — fell at least 20% from a peak within twelve months. Robinhood and Rivian fell roughly 90%. Even Zoom and CrowdStrike, which finished the year sharply higher, put their owners through declines of 40% or more along the way.

Source: Truist. Past performance is no guarantee of future results.

That is the discipline lesson in a single chart. Even when you manage to pick a genuinely good company, buying into the hype means accepting a violent ride — and, more often than not, the chance to own the same business at a lower price later on.

Full data: returns from the IPO

Source: Truist. Past performance is no guarantee of future results.

The Long Run Tells the Same Story

That three-year shortfall in the chart above is no accident. Decades of academic research have documented that, as a group, IPOs have tended to lag both the broader market and comparable, seasoned companies in the years following their debut. The reasons are intuitive. Lock-up periods eventually expire, releasing a wave of insider selling. Newly public companies often lack the long operating history that lets you judge quality. And many companies choose to go public precisely when sentiment for their story — and their valuation — is at its hottest. Buying at peak enthusiasm is rarely a recipe for strong long-term compounding.

Why Investors Get Caught

If the odds are this plain, why do investors keep reaching for the hot new issue? Because the pull is emotional, not analytical. The story is compelling, the coverage is everywhere, and the fear of missing out is real. This is the same recency bias and herd behavior we warn about elsewhere — the urge to chase what is exciting today rather than own what has proven durable over decades. It is classic bad investor behavior, and as the data above shows, yesterday’s most-hyped debut is very often tomorrow’s laggard.

None of this means you must swear off newly public companies forever. Discipline is not the same as avoidance. It simply means refusing to let a roadshow and a countdown clock make your decision for you. In practice, that looks like a few simple habits:

The Disciplined Approach

- Let the hype settle. There is rarely any reward for being first through the door, and often a penalty.

- Wait for real results. A few quarters of public, audited reporting let you judge the business on its numbers — not on a story.

- Demand quality and a sensible price. The price you pay determines the return you earn. A great company at a hype price can be a poor investment; that same company a year or two later, with a track record and a reasonable valuation, may be an excellent one.

The distinction worth holding onto is the one between a great company and a great investment. They are not the same thing, and the gap between them is usually the price of the hype. Durable results come from owning quality, owning it directly, keeping costs low — and refusing to chase. The opening bell makes for great television. It rarely makes for great investing. Stay the course.