When it comes to constructing a balanced investment portfolio, one crucial asset class is fixed income. Fixed income investments, such as bonds, serve as the bedrock of stability, providing a predictable stream of income and acting as a counterbalance to the volatility of equities.

Fixed income refers to investment securities that generate a fixed or predictable stream of income over a specified period. The most common types of fixed income investments are bonds, which are essentially loans made by investors to governments, municipalities, corporations, or other entities. These bonds typically have a predetermined interest rate, maturity date, and regular interest payments.

Pros of Fixed Income

Stability and Predictability

Fixed income investments, primarily in the form of bonds, provide a predictable stream of income and serve as a counterbalance to the volatility of equities. Bonds generate a fixed income over a specified period, offering a level of stability that can help cushion the impact of market downturns. This reliability makes them essential for constructing a balanced investment portfolio.

Capital Preservation

One primary objective of fixed income investments is to preserve capital. While equities are susceptible to significant fluctuations in value, bonds typically maintain more price stability over time. This characteristic becomes particularly beneficial during market turbulence when fixed income investments often retain or even appreciate in value because they provide a safe haven for investors.

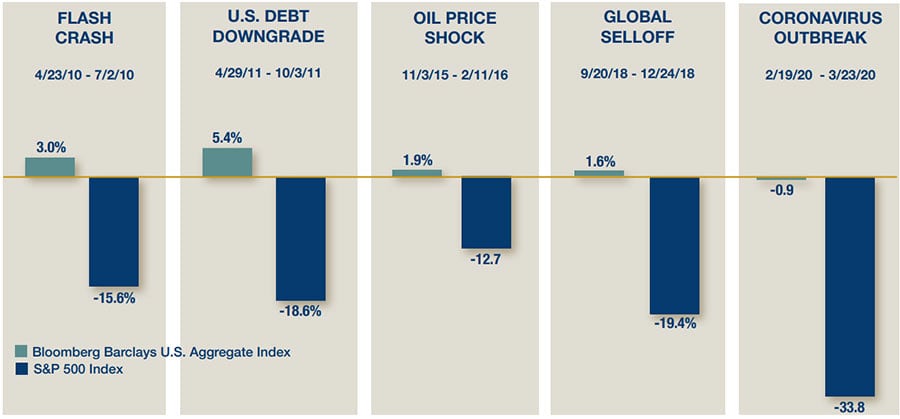

The below chart shows how bonds’ resilience can mitigate the pain of equity down-markets:

It is not possible to invest directly in an index. Indexes are unmanaged and do not reflect the deduction of fees or expenses. All investments are subject to risks, including the risk of loss. Past performance is not indicative of future results.

Diversification and Risk Mitigation

Adding fixed income to a portfolio adds diversification and risk reduction. When stock markets decline, fixed income investments generally exhibit less pronounced price fluctuations, acting as a stabilizing force. This dynamic reduces overall portfolio risk and smooths performance over time, allowing for a more balanced approach to investing.

While bonds can fail, they are generally considered safer investments than stocks. This is because the company issuing the bond is obligated to pay coupon payments and the face value at maturity. Even if the company fails, bondholders have priority over stockholders in recouping what they can from the failed company.

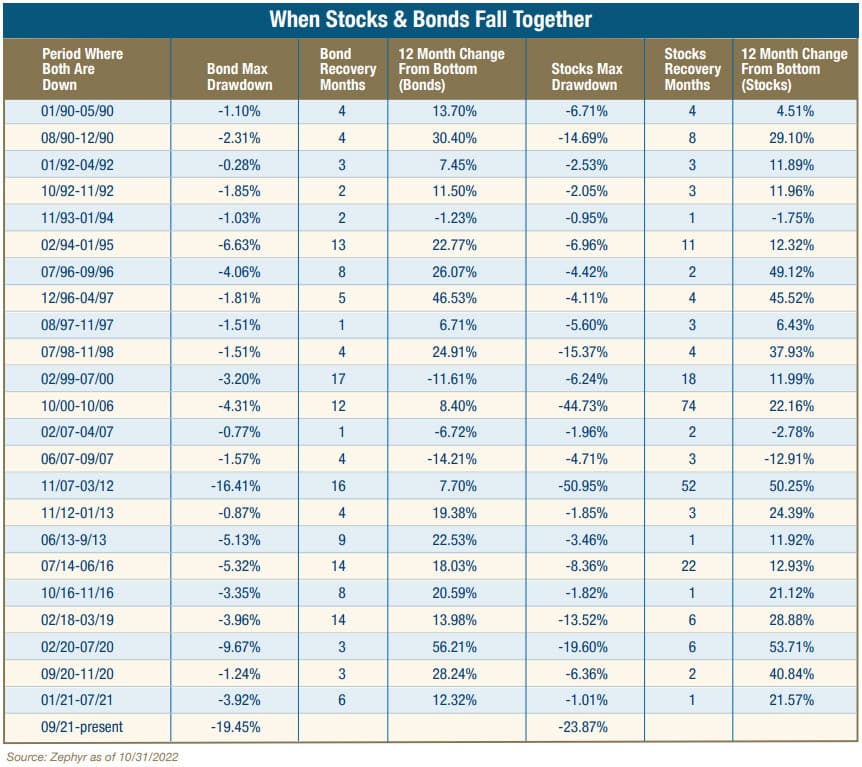

Sometimes bonds and stocks do decline together, but you can see from the chart below that bonds often recover their value much faster:

It is not possible to invest directly in an index. Indexes are unmanaged and do not reflect the deduction of fees or expenses. All investments are subject to risks, including the risk of loss. Past performance is not indicative of future results.

Regular Income Generation

Bonds are renowned for their ability to generate regular income through fixed interest payments, also known as coupon payments. This income stream is especially appealing to retirees seeking a reliable source of funds to meet their recurring financial obligations as it allows investors to fund their standard of living without relying solely on equity returns.

Long-Term Compounding

Investors can reinvest the income generated from bonds, enhancing long-term compounding. For instance, consistent cash flow from bonds during market downturns can enable investors to purchase additional bonds at lower prices, strengthening their portfolio over time. This strategy mimics the approach of accumulating rental properties, where income can be reinvested to generate further cash flow.

Adaptability to Interest Rate Changes

While rising interest rates can lead to declines in bond prices, the long-term outcome remains unchanged. Bonds mature at their face value, providing assurance to investors, and allowing reinvestment of the interest into new bonds. By reinvesting cashflow into new bonds with better yields, investors can enhance portfolio yield and cashflow, generating long-term financial benefits.

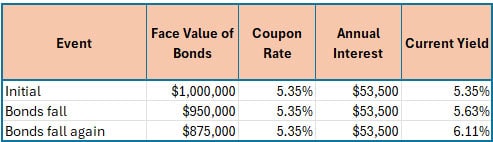

As the price of the bond falls, the yield increases. This is because the interest received via coupon payments remains constant, even as asset prices are falling. See the example below:

These are hypothetical figures.

Essential for Retirement Planning

Bonds are a critical component for creating income in retirement. A well-constructed bond portfolio can meet income needs without drawing down on equity principal, thereby helping preserve wealth for future generations. Incorporating bonds into a pre-retirement strategy builds a foundation for income security and stability.

Not only do bonds allow for long-term stability, but the income can help investors meet spending needs, allowing equities more time to grow. This can be especially useful in down markets because those who have all of their investments in equities must sell stocks at a loss to fund distributions that pay the bills. Having a balanced portfolio, with directly owned bonds, helps the investors when markets move up and preserves the portfolio when they move down.

Cons of Fixed Income

Limited Growth Potential

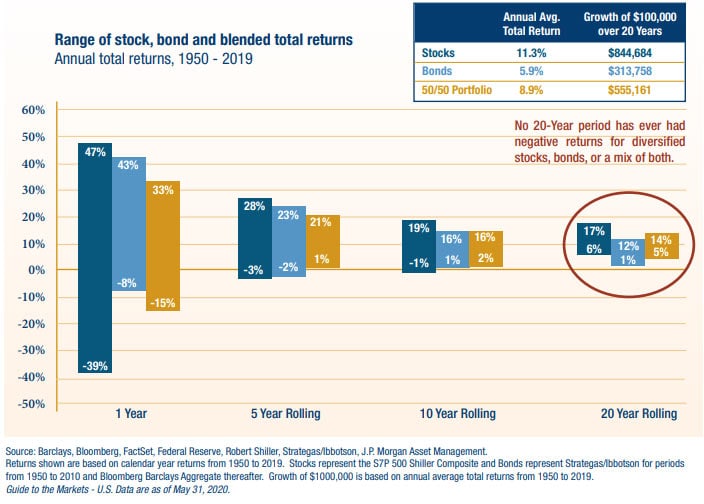

While fixed income investments are excellent for generating cash flow, they are not designed for growth. Historically, bonds have not outperformed equities, and their returns can be significantly lower. This limitation means that a balanced portfolio should also include an equity allocation to capitalize on growth opportunities. The chart below shows how stocks are volatile in the short term, while bonds are more consistent. On the other hand, stocks earn a higher return than bonds on average. A combination of stocks and bonds can help a portfolio experience growth while maintaining a relatively stable floor:

Source: Barclays, Bloomberg, FactSet, Federal Reserve, Robret Shiller, Strategas/Ibbotson, J.P. Morgan Asset Management. Results shown are based on calendar year returns from 1950 to 2019. Stocks represent the S&P 500 Shiller Composite and Bonds represent Strategas/Ibbotson for periods from 1950 to 2010 and Bloomberg Barclays Aggregate thereafter. Growth of $1,000,000 is based on annual average total returns from 1950 to 2019. Guide to the Markets – U.S. Data are as of May 31, 2020. It is not possible to invest directly in an index. Indexes are unmanaged and do not reflect the deduction of fees or expenses. All investments are subject to risks, including the risk of loss. Past performance is not indicative of future results.

Sensitivity to Interest Rates

When interest rates increase, bond prices decline, but coupon payments and payment at maturity don’t change. If you own bonds directly, and can avoid selling during a down market, then a decline in a bonds price (or resale value) shouldn’t impact you. However, if bonds are owned in a pooled fund, or if the investor needs to sell the bonds to meet short-term needs, interest rate increases can be detrimental to the investor.

Market Cycles and Timing Challenges

Bond cycles are notoriously difficult to predict. Attempts to time the market can result in missed opportunities for revenue generation. If investors hold cash while waiting for favorable conditions, they may experience revenue loss over time, highlighting the importance of consistent investment in bonds.

Perception of Discounts

Investors should approach discounted bonds with caution. A bond selling at a discount often indicates market skepticism about its value. While some discounts may present buying opportunities, they can also signal underlying issues that may affect returns.

Complexity of Bond Management

Managing a bond portfolio requires expertise and can be more complex than simply investing in pooled bond funds. Many investors may be unaware of the advantages of building a tailored private bond portfolio that aligns with their specific needs, potentially sacrificing long-term income and growth.

Institutional Direct vs. Pooled Ownership

If you believe in diversification, building a portfolio of bonds over time can be one of the best ways to ensure that you will have income at retirement. Academics have shown that holding bonds, owning them directly, and reinvesting the income over time can not only minimize risk but also enhance long-term returns. While having bonds in your portfolio seems like a no-brainer, it’s important to understand why bond funds or ETFs are often not suitable for affluent bond investors.

8 Reasons Affluent Investors Should Never Buy Bond Funds or ETFs

1. Pricing disadvantages

When buying into a bond fund, you are buying shares of the fund not the underlying bonds themselves. Because most bond funds own bonds that were bought years ago, many will have high premiums that may mean the yields to maturities are very low. In short, high bond prices with yield of 1% or 2% before fees are not very attractive.

2. Herding impact

Investors that go in and out of the fund during good and bad markets impact the managers’ selling and buying, which not just increases transaction costs but also hurts performance by selling low and buying high.

3. Expense ratio

This is when the fund or ETF charges an annual fee. Industry averages can be between .4% and 1%. The challenge is if the bonds average a yield to maturity of 2%, and the expense ratio before trading fees is 1%, then investors only net 1%.

4. Trading costs

One of the biggest mistakes investors make is thinking funds don’t charge for trading. Trading costs do increase overall cost, and the total impact is estimated to increase costs between .2% and 1.5% depending on turnover.

5. No maturity

Investors in bond funds have no maturity as they would by owning bonds directly. This poses a problem because if bond funds go down in value, and bonds are then sold, the investor’s ability to hold bonds to maturity and recoup principle doesn’t exist.

6. Advisor cost

If you use a financial advisor and he invests your money in a bond fund, he often will charge you an annual fee. Keep in mind retail advisors are not money managers and generally invest in funds that they don’t have the skills, expertise, or time to manage those investments themselves.

7. No direct ownership

You don’t own the bonds directly or have control of what the fund is buying.

8. Down market spreads

When down markets occur and small investors sell bond funds, the fund managers are often forced to sell bonds with deep discounts to create liquidity, which increases trading spreads. This can damage investor principal.

6 Reasons Linden Thomas & Co. Builds Each Bond Portfolio with Direct Ownership

1. Tailored to investor income needs

Each portfolio is tailored to the investor’s specific income, maturity and risk need.

2. Direct ownership

Our clients own the bonds directly, giving them total control and transparency.

3. No annual expense fee

All income goes directly to each client from the bonds they own, which not only increases net cash flow but also buying power.

4. Down market control

Because our clients owns each bond directly, when markets go down, adding shares results in a direct benefit.

5. No small investor herding impacts

Direct ownership avoids small investor herding impact found in pooled funds.

6. Easy to monitor net income needs and retirement goals

because each bond adds net cash flow, the investor’s net income is easily identified and tracked to ensure income is available at retirement.

Fixed income investments play a crucial role in a balanced portfolio, offering stability, predictable income, and diversification. However, investors must also be aware of the limitations and challenges associated with fixed income. By understanding both the pros and cons, investors can make informed decisions designed to optimize their portfolios for long-term success.

Related Articles

Are bond index funds efficient?

Fixed Income,

Index Investing,

Index Sectors,

Pros & Cons,

Top Fixed Income FAQs,

Top Index FAQs,

Types of Indexes,

October 23, 2023

Why to Invest in Bonds and Where to Buy Them

Fixed Income,

Why to Buy & Where,

September 24, 2024

How do Bonds Work?

Fixed Income,

How Bonds Work,

October 24, 2023