Index providers establish a set of criteria that securities must meet to be considered for inclusion in an index. In many indexes, the primary requirement for inclusion is market-capitalization, or the size of a company. Generally, indexes don’t pay attention to the earnings quality of companies, meaning companies can lose money for years before being removed. Securities are evaluated and ranked based on the selection criteria. After the evaluation and ranking process, the index provider constructs the index by selecting securities according to their respective weights.

Over time, companies that grow enough in size may be added to the index, while companies that shrink below a minimum requirement are removed. The companies in the index are updated regularly during a process called reconstitution. When a company is removed from an index, it is called a delisting. Delistings can have a significant impact on performance.

Reconstitutions

When a stock is removed, index providers typically replace it with another eligible security that meets the inclusion criteria. This rebalancing process may require selling the delisted stock and purchasing the newly added security, leading to transaction costs and potential market impacts. Additionally, the replacement security may have a different risk and return profile, which can alter the overall risk and performance characteristics of the index.

Mutual funds make distributions to shareholders for taxable realized capital gains generated within the fund. These taxable realized capital gains result from rebalancing, index reconstitution, or position closure related to share redemptions. The mutual fund structure often lends itself to more frequent taxable events, because they must often liquidate securities to cover shareholder redemptions. Any time securities are sold for a price higher than their cost-basis, capital gains are generated and taxes must be paid on the appreciation.

Realized net capital gains are passed along to existing shareholders, which can force newer shareholders to pay taxes on appreciation they never received. This can be doubly painful when the value of the fund is down overall, but taxes are still due.

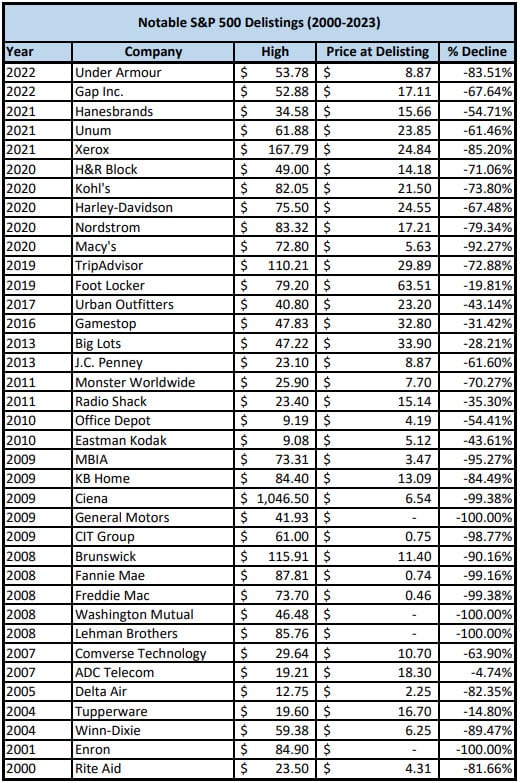

Delistings & Performance

Delistings, or the removal of stocks from an index, can have a considerable impact on index performance. A company can be delisted from an index for several reasons, such as a merger, acquisition, bankruptcy, or failure to meet listing requirements.

Delistings can distort the performance of an index, especially if the removed stock has experienced significant price fluctuations. If a delisted stock performed exceptionally well or poorly before its removal, its absence from the index can create a distortion in the overall index performance, potentially skewing the returns and characteristics of the index.

When a shrinking company falls below the requirements it is removed from the index, and any losses are realized. This, along with small-investor herding impacts and hidden costs, are often more impactful during down-markets and recessions.

For example, imagine a portfolio has 10 stocks all at $10/share and a total value of $100. If the market drops 20% and the value drops to $80, then each share needs to recover $2 to get back to $10 and break even. Now imagine that one of the shares is for a company that goes bankrupt. You only have 9 shares left, and they need to grow 28%, rather than 20%, to break even. In other words, quality impacts may not be represented as part of the expense ratio but should be carefully considered when investing in pooled market-cap index funds.

Enron’s delisting in 2001 is good example of why only considering a company’s size can be perilous. Once a darling of Wall Street, the company was a major constituent of the S&P 500 Index. When its accounting fraud was uncovered and the stock price collapsed, index funds holding Enron suffered immediate losses. Enron was only removed from the S&P 500 index a few days before filing for bankruptcy, meaning the index did not reconstitute in time to prevent index investors from suffering losses.

Direct Indexing

Due to the shortcomings of pooled market-cap index funds, many investors prefer earnings-focused direct indexing. Rather than buying pooled products like mutual funds and ETFs, investors can buy individual stocks and/or bonds, thereby circumventing some of the pooled products’ shortcomings. This is why Linden Thomas & Co. built earnings focused institutional indexes by applying earnings quality screens. Direct indexing allows investors to screen for earnings quality. By excluding companies with poor earnings quality, investors can hope to avoid the unhealthy companies included in the index.

The reconstitution of indexes is a vital process to ensure their relevance and accuracy in reflecting the market landscape. The removal of stocks through delistings can significantly impact index performance, introducing distortions, requiring rebalancing adjustments, and affecting investors who utilize pooled index-based investment products. It is crucial for investors to understand the mechanics of index reconstitution and stay informed about the changes to effectively navigate the ever-evolving investment landscape. By recognizing the impact of delistings, investors can make informed decisions and adapt their strategies accordingly while pursuing their financial objectives.

Related Articles

What are Mutual Fund Inefficiencies?

Index Investing,

Indexing for the Affluent,

Investment Principles,

Top Investment Principles FAQs,

November 19, 2024

What is the Real Turnover of Pooled Index Funds?

Index Investing,

January 8, 2025

How delistings impact investment results, especially when it comes to index funds

Index Investing,

October 15, 2024