When it comes to retirement planning, individuals often focus on the preparation. Building a portfolio and accumulating assets in your working years is essential to having confidence in your portfolio in your golden years. There should also be a heavy emphasis on savings, spending, and investment discipline as well. Saving habits, spending discipline, and portfolio management are what we consider the “Big 3.” When a client does a good job in these areas, these three factors work together over time to better ensure that he or she has sufficient savings and investments once they leave the workforce. We call this “finishing well.”

While finishing well is important, “ending well” is equally important. You don’t want to deplete the portfolio in your retirement years, putting yourself in a position where you have significantly less spending capital. This is especially true because, unlike during your prime earning years, your ability to go back to work may be limited. When you also consider the fact that healthcare costs become a larger focus as you get older, as well as the effects inflation may have on your overall portfolio, and expenses it becomes essential that the same discipline that helped prepare you for retirement will be needed to sustain you after retirement.

A healthy retirement starts with a well-balanced portfolio. Being invested in an efficiently managed portfolio can properly position you for the ups and downs of the market. The next step is having a conservative distribution rate. This is where the 4% rule applies.

A general principle in the investment community is that retirees should live by the 4% rule. This is a widely accepted recommendation that annual distributions from your investments should not exceed 4%. This is because distributions larger than 4% have the potential to be greater than your gains, which will result in you removing some of your principle. This will cause the account to deplete over the long term, putting you in danger of getting to an advanced retirement age with little to no savings left.

While 4% is considered the glass ceiling of distributions, ideally, your distribution rate should be lower than 4%. Why? Assuming you have a healthy, well-balanced portfolio, a lower distribution percentage allows more of your investment gains to work for you, resulting in your retirement account being better positioned for more gains. This is important when you consider external factors such as inflation, increasing healthcare costs, and other unexpected expenses you may face. Retirement is not the end of your story. Increasing life expectancy means that many people are living longer in retirement. Portfolio discipline, as well as conservative distributions, better equip you for whatever life brings.

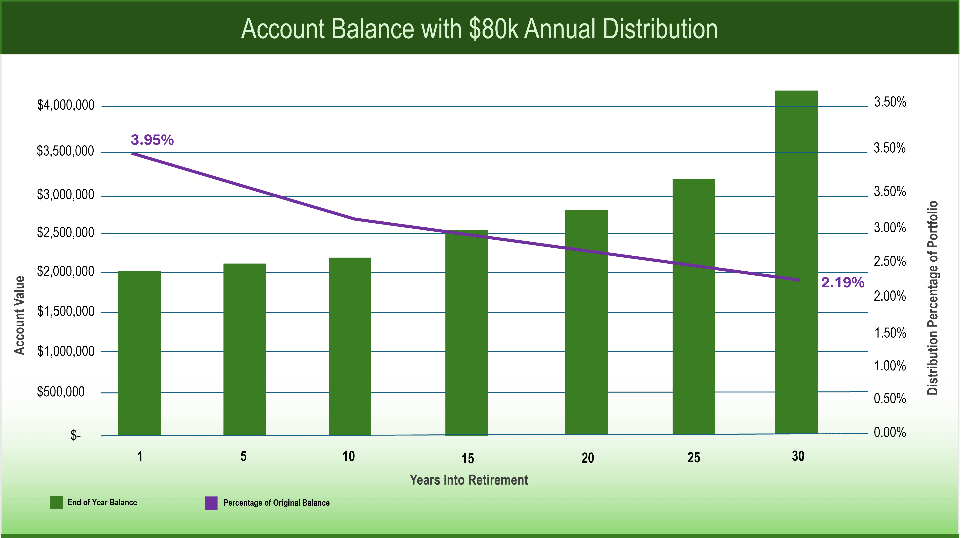

To help demonstrate this, the chart below demonstrates the hypothetical effects of following the 4% rule. For this example, we will assume the client has a balanced portfolio, with investments in healthy companies across various sectors. We will also assume the client is receiving average return. At retirement, the client is starting with 2 million dollars and decided upon retirement to take out $80,000 a year, aligning with the “glass ceiling” distribution rate of 4%:

The client’s adherence to a conservative distribution rate allows for the account (in this example) to continue its growth trajectory, even through retirement. As the client advances in retirement age, the account continues to modestly grow as well, which is essential for the ability to deal with any unexpected expenses due to inflation, healthcare costs, or other concerns. Another important note is that the $80,000 annual distribution, which started out as 4% of the portfolio, drops to only 2.19% of the portfolio by the time you get to 30 years after retirement. This illustrates the lasting effects the conservative distribution had on the overall portfolio.

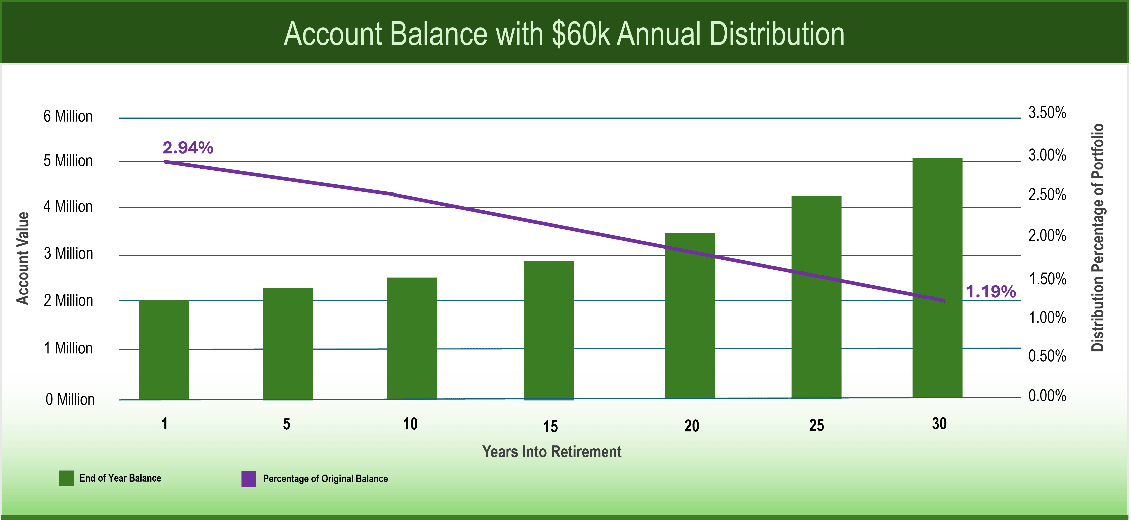

While we can clearly see the positive outcomes of adhering directly to the 4% distribution rule, an even more conservative distribution rate can produce even more positive results. Here are the lasting impacts of the same balanced portfolio with a 3% rate of distribution, which is $60,000 a year.

While the 4% distribution rate paved the way for modest gains, a 3% distribution better positions the portfolio due to a larger percentage of your investment gains being reinvested. This allows for far greater growth potential. As the account grows, the $60,000 annual distribution becomes a much smaller percentage of the portfolio. This is why a distribution rate of 3 – 3.5% is ideal! Small differences in the rate of distribution can have massive implications for the overall value of the portfolio.

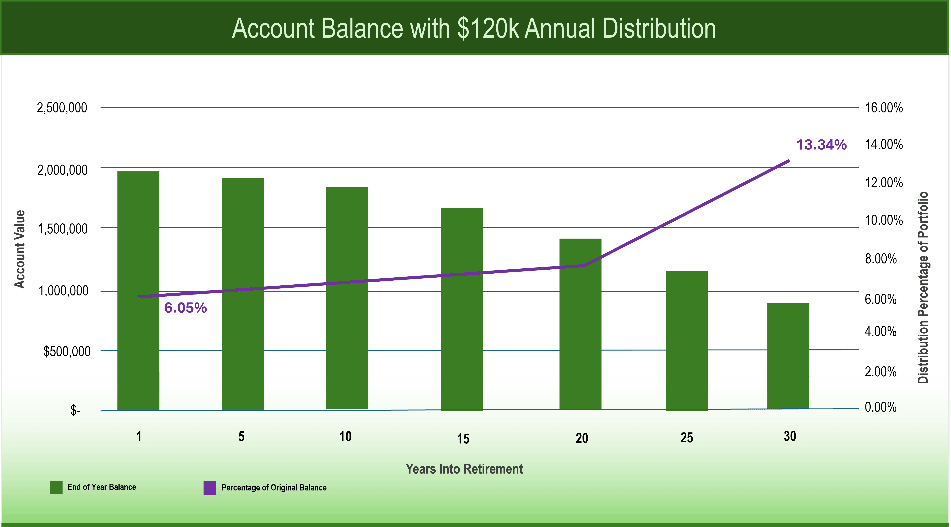

Similar to the way more conservative distribution rates have positive impacts on a portfolio, larger distribution rates have potentially devasting implications. To demonstrate this, notice the consequences of the same $2 million dollar portfolio, but the client is taking a $120,000 annual distribution, which equates to 6% of the portfolio.

While both the 3% and 4% distribution rates positioned the client to experience growth in the portfolio over the years, the 6% distribution rate caused the client’s account to decrease significantly, ultimately eroding more than half of the overall account value in 30 years. As a result, the $120,000 annual distribution became a much larger percentage of the overall portfolio, going from 6% to over 13%! As constructed, the client is now less empowered to deal with any potential unexpected expenses that may arise as they advance in retirement.

Preparing yourself for retirement through portfolio management and fiscal responsibility is very important. Demonstrating these same characteristics through retirement can play a vital role in the quality of your golden years. Having a distribution rate below the industry recommendation of 4% best positions your portfolio to continue working for you.

Related Articles

When should I start taking Social Security?

Financial Planning,

Personal Finance,

Top Personal Finance FAQs,

July 24, 2024

RMD Timing Secrets: When to Withdraw for Maximum Gains

Behavior,

Investment Principles,

Personal Finance,

Tax,

September 17, 2024

Why is Income Important in Retirement?

Fixed Income,

Personal Finance,

Top Personal Finance FAQs,

Why to Buy & Where,

August 14, 2024