By Indexopedia Research Team | December 10, 2024 | In

Compounding is one of the most powerful tools in wealth building. By allowing returns to generate additional returns, it creates a snowball effect that can significantly enhance an investor’s portfolio over time. However, compounding can also work in reverse when markets decline, and this negative compounding can likewise drastically reduce long-term portfolio growth. Fortunately investors can mitigate these dangers and potentially position themselves to rebound more quickly from market downturns.

The Harmful Impact of Negative Compounding

When a portfolio loses value during a down market, the math to recover becomes much more challenging. A 20% loss, for example, requires a 25% gain just to break even. A 50% loss? That demands a 100% gain to recover. This is the essence of negative compounding–the deeper the loss, the harder it is to regain the lost ground.

Consider an investor with a $2 million portfolio. A 30% market drop would reduce the portfolio to $1.4 million, and a 43% gain would be needed to restore the portfolio to its original value. This is a tough ask during times of economic instability, but there are strategies that can help minimize such damage.

Quality Investments as a Hedge Against Losses

Investing in high-quality stocks is a powerful way to help minimize the effects of negative compounding. Quality companies–those with strong balance sheets, dependable earnings, and durable competitive advantages–tend to be more resilient in volatile markets. Even during periods of sharp declines, these companies, while not guaranteed, generally experience smaller losses and are quicker to recover once the market rebounds.

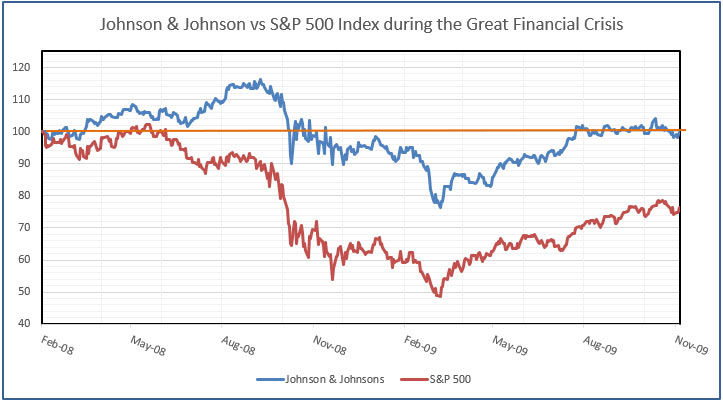

Take the 2008 financial crisis as an example. The broad market, represented by the S&P 500, lost 37% of its value. However, quality stocks like Johnson & Johnson and Procter & Gamble held up much better, losing around 8% and 15%, respectively. While many investors panicked and fled the market, those who held onto these high-quality companies experienced far less damage and were better positioned to capitalize on the eventual recovery. The chart below (Exhibit 1) illustrates this concept by plotting the performance of both the S&P 500 Index and Johnson & Johnson during (and immediately after) the Great Financial Crisis of 2008-2009. You can see how J&J did not suffer as deep a loss as the broader market. In addition, you can see how J&J’s quicker recovery time allowed it to outperform the S&P 500 even years after the initial crisis.

Exhibit 1 (Source: Factset) (an index is unmanaged, and you cannot directly invest in an index)

Direct Investing: Cushioning Against Market Turbulence

In addition to focusing on quality investments, direct investing offers another layer of protection against the dangers of negative compounding. Direct investing allows investors to purchase individual securities rather than pooling their money in funds such as mutual funds or ETFs. This provides two key benefits that can help safeguard portfolios during down markets.

First, direct investing eliminates small investor herding. In pooled funds, when a large number of investors rush to sell during a downturn, fund managers are forced to sell securities to meet redemptions. This mass selling can drive down the price of the underlying securities even further, exacerbating losses for all investors. In contrast, direct investors are not exposed to this herd behavior. They have control over when and whether to sell their holdings, allowing for a more measured response to market volatility.

Direct investing helps remove layers of costs like expense ratios, indirect trading fees, and pass-through taxes.

For example, during the dot-com crash in the early 2000s, many mutual funds that had heavily invested in speculative tech stocks were decimated. However, direct investors who had significant exposure to quality companies like Microsoft saw far smaller losses. Microsoft’s strong fundamentals allowed it to recover swiftly, and investors who held on were eventually rewarded with significant long-term gains.

Reducing Recovery Time

Quality-focused investments not only minimize the immediate impact of market declines but also shorten the time it takes to recover. While lower-quality, more speculative stocks may take years to rebound (if they recover at all), high-quality companies tend to bounce back faster once the market stabilizes. This reduces the drag of negative compounding and could allow the portfolio to resume its growth trajectory sooner.

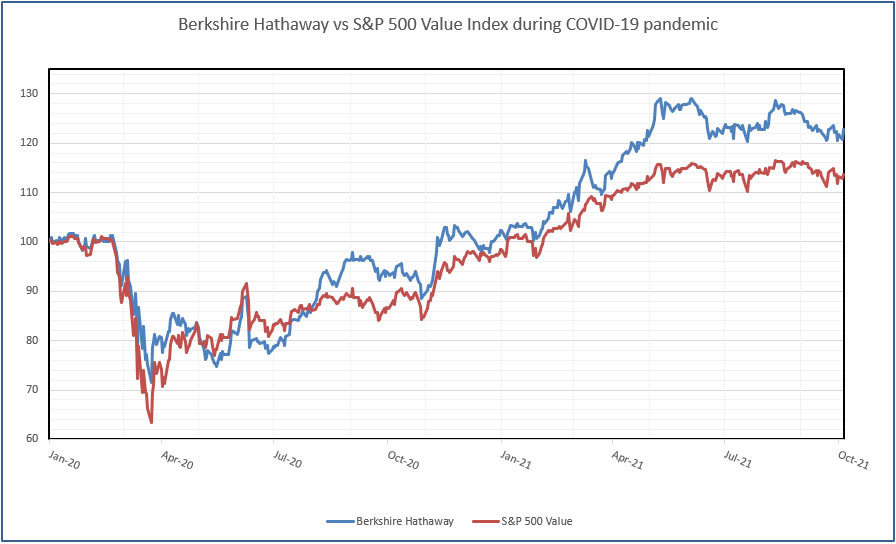

Take the example of Berkshire Hathaway during the 2020 COVID-19 market crash. While the broader market experienced dramatic volatility, Berkshire’s portfolio of quality holdings saw more muted losses. As the market recovered, Berkshire’s stocks generally rebounded faster, reducing the overall impact of the downturn on long-term portfolio growth. In contrast, more speculative investments, such as many small-cap growth stocks, took far longer to recover or failed to recover entirely. Exhibit 2 demonstrates how Berkshire was able to quickly recover from the COVID-19 pullback and ultimately outpace the broader market throughout the remainder of the next 18 months.

Exhibit 2 (Source: Factset)

(an index is unmanaged, and you cannot directly invest in an index)

Compounding Through Quality

We believe, the long-term compounding effect is the true driver of wealth creation, and preserving it during down markets is critical. High-quality companies with strong fundamentals, while not guaranteed, have a proven track record of delivering consistent returns over time, even in the face of economic challenges. By maintaining a portfolio of quality stocks, investors are better positioned to achieve steady compounding and reduce the impact of negative compounding during downturns.

For example, consider Johnson & Johnson, a company that has been paying dividends for decades and has consistently increased its dividend payouts, even during economic recessions. Investors who reinvested those dividends over time benefited from compounding returns, regardless of short-term market fluctuations. This type of resilience is what allows a portfolio to grow steadily, even in the face of temporary setbacks.

Planning for the Next Down Market

While no one can predict the future, investors can plan for it by focusing on quality investments and employing strategies like direct investing. By minimizing exposure to speculative assets and avoiding the herd mentality that drives panic selling, investors can help protect their portfolios from the worst effects of negative compounding.

In the end, down markets will come and go, but a portfolio built on quality is much better suited to weather the storm and emerge stronger on the other side. The key is to stay disciplined, invest in resilient companies, and ensure that negative compounding doesn’t stand in the way of long-term wealth creation.

Related Articles

What are Rallies, Pullbacks, and Average Returns?

Investment Principles,

Top Investment Principles FAQs,

Understanding Results,

November 3, 2023

What Happens When Average Returns Flip?

Markets,

February 11, 2025

What If You Miss the Best Part of the Recovery

Investment Principles,

Markets,

Top Investor Mistakes,

August 12, 2024