Market rallies come in all flavors and sizes. Sometimes a broad index like the S&P 500 or the NASDAQ rallies. Other times, a specific economic sector — Technology and Communications, or Energy and Commodities — breaks out. And in yet other circumstances, a group of businesses benefiting from some trend or theme — the Nifty 50, the Dot-Coms, or the Mag 7 — will rally. Rallies are great while they last, but inevitably they give way to corrections, and sometimes to bear markets. Then the road to recovery begins.

All too often, investors focus on a narrow portion of the cycle (typically the rallies) and ignore the rest — the declines and the recoveries. Yet all three components are what produce returns over time. This is what we call a full market cycle. And it is vital to your future success in investing to ensure your behavior is consistent with how markets actually work.

Prediction vs. Participation

Some investors focus on predicting turning points — trying to find the next index, sector, or theme set to rally. Others develop schemes for the right time to sell. Not only do these investors have to get the economics right and the trend right, but they also have to get the timing right. And then, once they have it figured out, they have to execute it better than everybody else.

Study after study has demonstrated that nobody can reliably predict the trend, the timing, or the turning points — because nobody can predict the future. In short, timing rallies is a fool’s errand. But does that stop people from trying? Of course not. To many longtime market watchers, the casino-like atmosphere on Wall Street is getting more popular by the year. But investing isn’t a casino. It’s the ownership of businesses that enables your money to make money for you. Because of that, it is wiser to participate, rather than predict. The level of success you ultimately enjoy as an investor hinges entirely on your perspective and discipline.

The Trap Hidden Inside Average Returns

Here is one of the most under-appreciated traps in all of investing: trailing average returns look their absolute best at exactly the wrong moment to invest. Recent strong performance — the kind that finally gets your attention, dominates the headlines, and fills the cocktail conversations — is also what may mark the late stage of a rally. Recency bias takes the wheel. The rear-view mirror feels like a windshield.

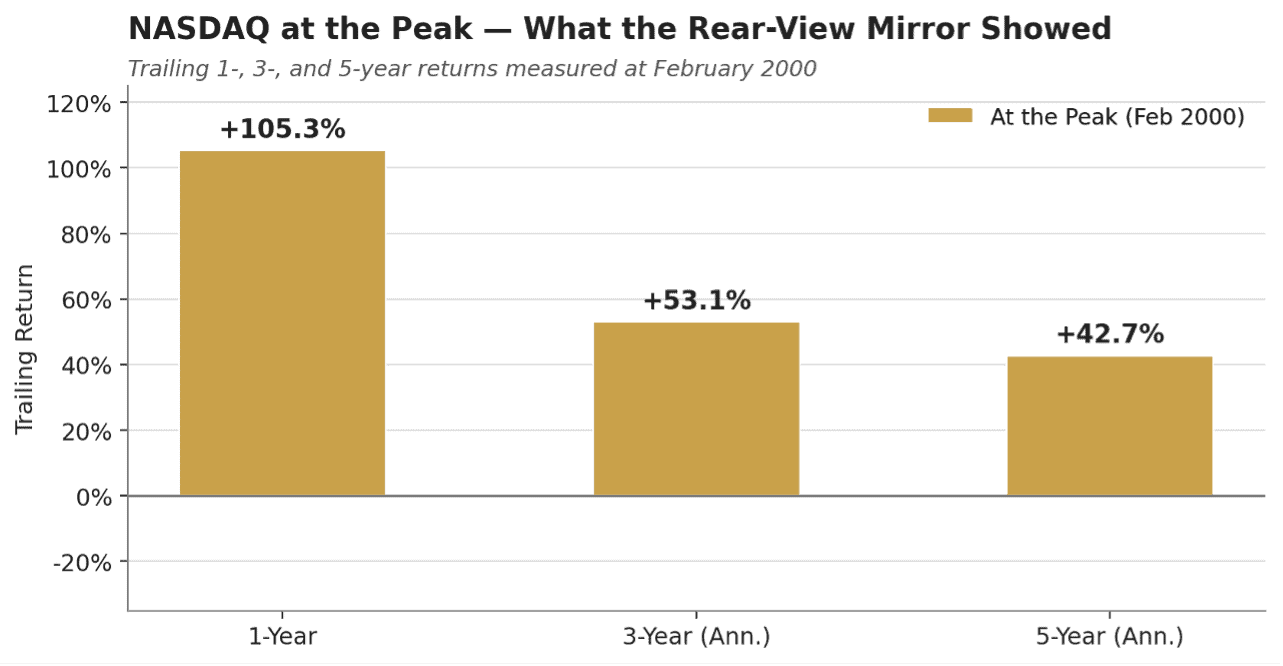

Consider the NASDAQ at the peak of the Tech Bubble in February 2000. An investor evaluating the index on that day would have seen the trailing 1-year return at +105.3%, the 3-year annualized at +53.1%, and the 5-year annualized at +42.7%. The data could not have looked more inviting. Headlines screamed about a new economy. Cab drivers gave stock tips. Walking past this opportunity felt foolish.

Source: Factset. Trailing returns for the NASDAQ Composite measured at the bubble peak in February 2000.

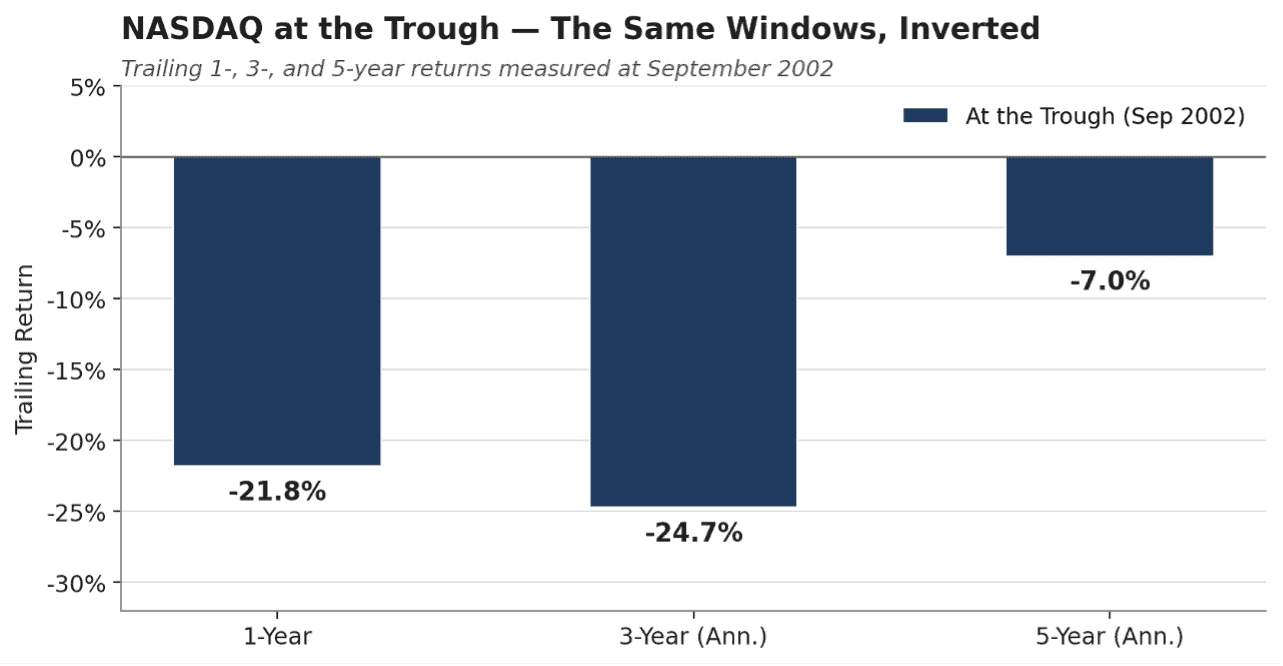

By September 2002 — just thirty-one months later — those same trailing windows had inverted, as shown below. The 1-year return was -21.8%. The 3-year annualized was -24.7%. Even the 5-year annualized, which had captured the euphoric run-up, was negative at -7.0%. The investor who chased the rally in early 2000 didn’t just give back the gains they hoped to capture — they bought at a high price and then watched in real time as the very averages that lured them in went red.

Source: Factset. The same 1-, 3-, and 5-year windows, now measured at the NASDAQ Composite trough in September 2002.

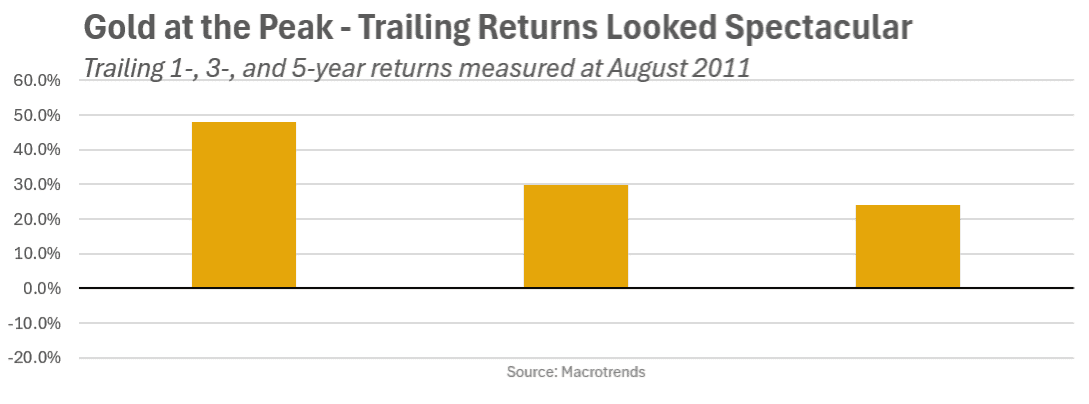

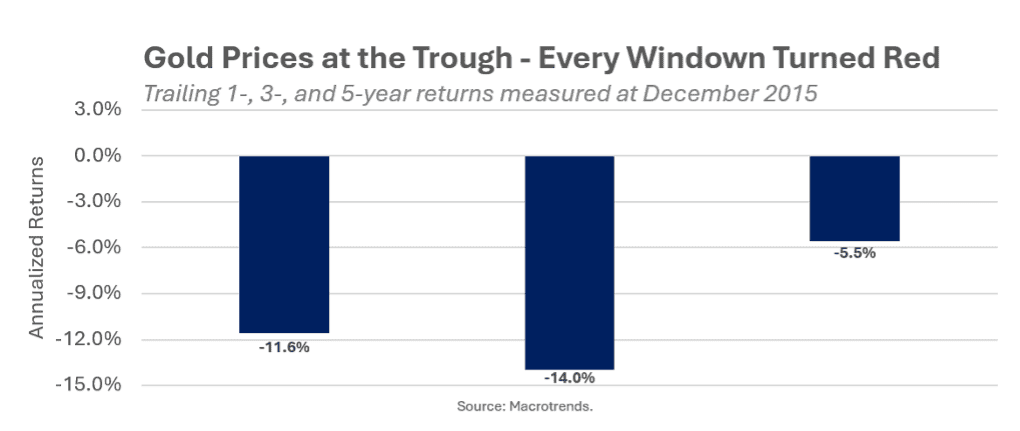

This isn’t a one-off. The same dynamic played out in gold a decade later. Gold rallied for years on inflation fears and a weakening dollar, and by August 2011 the trailing returns looked spectacular: +45.6% over 1 year, +29.6% annualized over 3 years, and +23.3% annualized over 5 years. Investors flooded in. Pundits declared a new monetary regime.

Then came the bear market. By December 2015, gold had given back years of gains, and the same trailing windows that drew investors in had flipped negative across the board — exactly as they had for the NASDAQ thirteen years earlier.

Different asset. Different decade. Same behavioral pattern. The investor who waited until the trailing returns looked irresistible was the investor who handed their capital to the previous holder at a horrible price.

Why Chasing Feels So Compelling

Rallies create powerful psychological pressure. Watching friends, coworkers, or media personalities make easy money triggers FOMO — the fear of missing out. The recency effect takes over. Recent strong performance feels like it will continue forever. The longer the rally runs, the harder it gets to keep a bridle on your enthusiasm. There is perhaps no greater test of investor discipline than a powerful market rally.

As prices climb and headlines scream about new highs, something strange happens: rational people begin to act irrationally. They abandon carefully constructed plans and start chasing returns they’ve already missed. We call this Rally Behavior — and it remains a reliably destructive force in investing.

As prior articles in this series have shown:

- Average returns lie — they are backward-looking and heavily influenced by recent performance.

- Sector rotation is real — today’s winner is often tomorrow’s loser.

- Chasing hype is one of the most common — and costly — investor mistakes.

The History Is Brutal

Buying late in a rally doesn’t just reduce your upside — it dramatically increases your downside risk. You are buying near peak optimism, peak valuations, and often peak leverage. When sentiment eventually turns, the fall is sharper and the recovery takes longer. That harms your ability to compound at satisfactory rates over time.

Most recently, the AI theme has rallied massively. It has not yet reached the pinnacle of the Tech Bubble of 2000, and it certainly hasn’t experienced a meaningful correction. Like every rally before it, an AI correction will come. It is inevitable. But there is no telling when.

The Core Problem: You’re Buying the Returns Someone Else Already Earned

When a rally is in its early and middle stages, the biggest gains are usually already made. By the time the late-entry investor notices and feels the urge to get in, they may no longer be getting a bargain. They are buying momentum at elevated prices. The trailing returns they’re staring at — the ones that finally convinced them to act — are precisely the returns the early investors are now preparing to sell to them.

This is the fundamental stupidity of chasing rallies:

- You are paying a premium for returns that someone else has already collected.

- You are voluntarily taking on higher risk for lower prospective returns.

- When the correction occurs, the pain often forces you to sell — locking in losses near the bottom.

The later you enter, the worse the risk-reward equation becomes. The pattern is always the same: the later you chase, the more pain you eventually feel.

A Smarter Alternative

Instead of chasing rallies, do the opposite:

- Stay disciplined during strong markets — don’t let trailing returns lure you into late-stage entries.

- Use volatility and corrections as opportunities to buy quality at better prices.

- Focus on time in the market, not timing the market.

A thoughtfully constructed portfolio built on earnings quality, direct ownership, and spreading risk gives you exposure to multiple sectors and asset classes. You don’t need to chase the current winner. You already own pieces of tomorrow’s winners at yesterday’s prices.

Final Thought

Rallies are seductive. They make otherwise intelligent people believe they’ve discovered a new paradigm. But the data, the history, and the math are clear: chasing late-stage rallies is one of the most expensive mistakes an investor can make. The truly successful investors are not the ones who ride every wave of euphoria. They are the ones who maintain discipline when others are losing their heads — and who have the courage to act when others are afraid.

Anchor your portfolio in the earnings power of the businesses you own, and judge results across the full market cycle — the ups, the downs, and the recoveries that follow. This is how satisfactory long-run returns are manufactured. Not by guesswork. And certainly not by chasing the hot dots.

Don’t chase the rally. Let the rally come to you — after it has shaken out the weak hands and created real value again.