Small Cap Value — and the Discipline to Own What the Crowd Won’t

For more than a decade, the market’s attention has been captured by a small group of large-cap growth companies — first the so-called “Magnificent Seven,” and more recently anything connected to artificial intelligence. The returns have been remarkable, the headlines louder still, and the gravitational pull toward those names has been almost impossible for the average investor to resist.

That’s the part everyone sees. What goes largely unnoticed is what has been quietly happening on the other side of the market — in the companies few are talking about, in a segment of the market many investors have stopped looking at altogether.

While the financial media has been busy chasing the shiny object, an entire asset class — small-cap value — has been doing exactly what disciplined investors are supposed to want: trading at reasonable valuations, compounding earnings, and quietly delivering. Oftentimes, opportunities are found by being willing to look where the crowd isn’t.

The Market Has a Short Attention Span

It’s hard for many investors to accept, but the market does not relentlessly process every publicly traded company with clinical objectivity. It has a narrow attention span — and the object of its affection is usually equally narrow. So it is a rule, rather than an exception, that the market gets fixated on something exciting while ignoring genuine opportunities elsewhere.

Today, that something is large-cap technology and AI. There is nothing wrong with owning those companies — many of them are exceptional businesses, and part of several Linden Thomas growth indexes. The problem is what happens to the rest of the portfolio when an investor’s attention, and capital, is concentrated almost entirely in one corner of the market. History has been unkind to investors who have abandoned discipline and balance by following the hot dot.

What Small-Cap Value Actually Is

Small-cap value companies are smaller businesses — typically those with market capitalizations under roughly $5 billion — trading at lower valuations relative to their earnings, book value, or cash flow. They are often described as boring: regional banks, manufacturers, energy companies, industrial businesses. They don’t dominate the headlines, and they rarely trend on social media.

That, by the way, is precisely the point. The premium for excitement has historically been one of the most expensive things investors pay for. The discount on the unexciting has historically been one of the ways investors get compensated.

Why It’s Been Out of Favor — and Why That Matters

For more than a decade, a unique combination of near-zero interest rates, easy money, and concentrated leadership pushed capital relentlessly toward large-cap growth. The market rewarded scale, network effects, and narrative. Small, profitable, unloved businesses were generally left behind — not because their fundamentals deteriorated, but because attention drifted elsewhere.

History shows that this dynamic does not last forever. When valuations stretch far enough, the market eventually rotates. And the rotation, when it comes, tends to happen faster than expected — and often before the headlines acknowledge it.

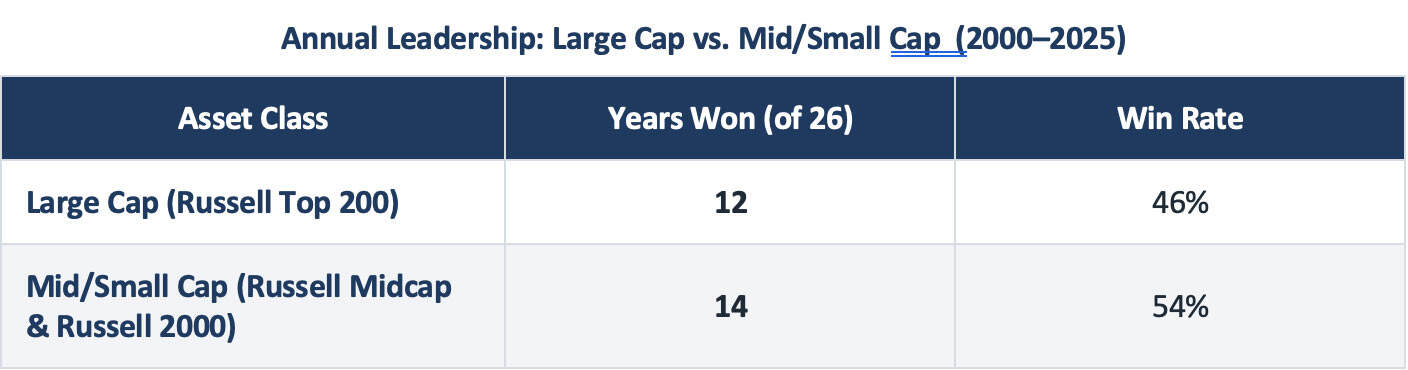

History Shows the Leadership Doesn’t Stay Put

One of the most useful exercises any investor can do is to look back over a long period and ask a simple question: who actually won? Not in the headline-grabbing year, but year after year, across cycles. When you do that exercise with large-cap and mid/small-cap stocks over the past 26 years, the result is not what most investors expect.

Source: FactSet. Indexes used: Russell Top 200 (Large Cap), Russell Midcap, and Russell 2000 (Mid/Small Cap). Annual leadership reflects the index with the highest calendar-year total return for each year from 2000 through 2025. “Mid/Small Cap” years are those in which either the Russell Midcap or Russell 2000 outperformed the Russell Top 200.

Out of the last 26 calendar years, large cap led the market in 12 of them. Mid- and small-cap stocks led in the other 14. The headlines of recent years would have investors believing the opposite. That gap — between what the market has actually rewarded over time and what investors believe it rewards — is exactly where bad behavior comes from.

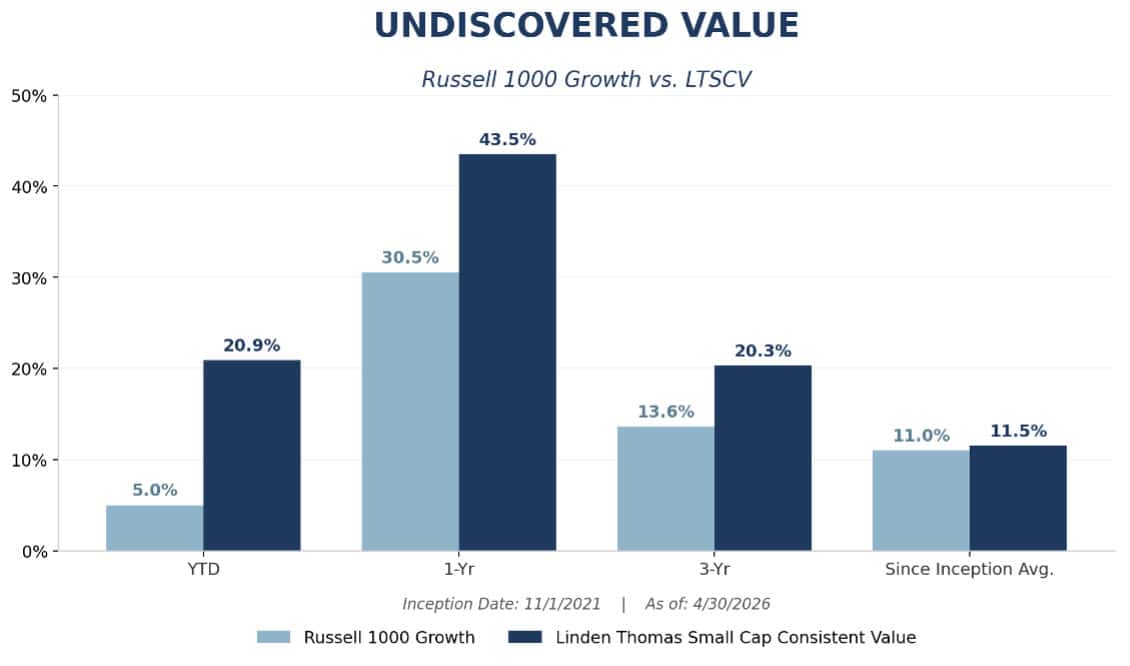

Undiscovered Value: The Linden Thomas Small Cap Consistent Value Index

While many investors remain transfixed by large-cap technology and AI, the Linden Thomas Small Cap Consistent Value Index (LTSCV) has been doing what disciplined small-cap value should do — quietly, and effectively. The comparison below shows LTSCV against the Russell 1000 Growth Index, which is a segment of the market that has dominated investor attention.

Source: FactSet. Inception Date: 11/1/2021. As of: 4/30/2026. Performance shown for periods greater than one year is annualized. All returns are net of 0.85% management fee. Past performance is not a guarantee of future results. Indexes are unmanaged and you cannot directly invest in an index.

The takeaway is not that large-cap technology or AI companies are bad investments, or that an investor shouldn’t own them. The takeaway is that the narrow paradigm the market and the financial news media offer — a story dominated by a handful of names — is not the same as a complete portfolio. Breaking free of that paradigm can dramatically improve long-term results.

The Behavioral Challenge

The hard part of small-cap value is not the math. The math is straightforward. The hard part is the behavior it requires. To capture this opportunity, an investor has to be willing to:

- Own stocks (or an index fund) that feel quiet — sometimes for long stretches.

- Ignore the constant narrative around whatever is hot at the moment.

- Stay invested through multi-year periods even when an unloved part of the portfolio lags the headlines.

Many investors cannot do that. They buy what is working and sell – or refuse to own – what isn’t. It may be the single most expensive habit in investing, and it shows up in every cycle.

How to Put It to Work

- Direct indexing: Owning the underlying stocks in an index may be the cleanest way to access the asset class. An added benefit is this method helps avoid the hidden fees, embedded costs, and tax inefficiencies found in traditional mutual funds.

- An earnings-oriented approach: An portfolio built around businesses that generate real earnings, not stories about potential ones.

- A measured allocation: A meaningful allocation – typically 10 – 20% of your equity allocation – that is held with discipline rather than chasing after a strong quarter.

Final Thought

Great investment opportunities rarely arrive with fanfare. They tend to show up when others are looking the other way – when the asset class in question feels dull, when the headlines are dominated by something more exciting, and when the easiest thing to do is nothing.

Small-cap value may not be flashy. And it may not make anyone the most interesting person at a dinner party, especially in a year when AI is in the news. But the long arc of market history is unambiguous about this: the investor who has the discipline to buy what few are buying today is often the investor who is rewarded tomorrow.

The question is simple. Are you willing to invest in what few are buying right now?

Related Articles

Rose Colored Glasses: Why Investing During the Good Times Can Create Poor Allocation Tilts

Investment Principles,

Top Investor Mistakes,

March 6, 2025

Waiting for Recovery Instead of Chasing Returns

Investment Principles,

January 8, 2025

Investor Fatigue – How to Avoid It

Personal Finance,

April 16, 2026