Don’t Let Wall Street’s Milestones Become Your Master

In June of 2026, Space Exploration Technologies Corporation (SpaceX) completed an initial public offering valuing the company at $1.8 trillion – the largest IPO ever. The company’s founder Elon Musk still owns 42% of the shares, valuing his interest in the firm at ~$756 billion. Combined with his other holdings of Tesla, xAI, the Boring Company, Neuralink and some smaller private holdings, Mr. Musk has famously become the first human being ever to achieve trillionaire status – with a combined net worth of approximately $1.2 trillion.

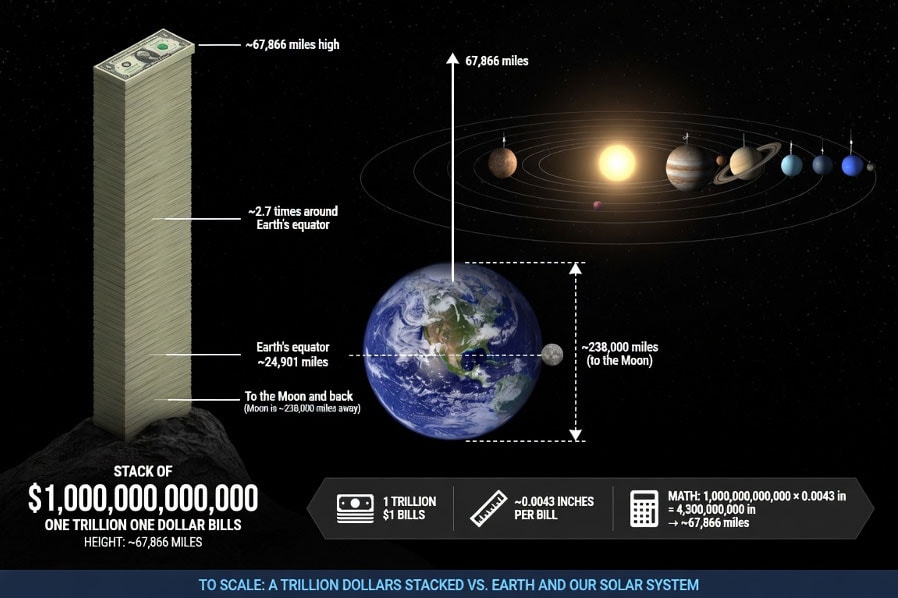

So, just how much is a trillion dollars? Well, for starters, a stack of a trillion, one-dollar bills would be more than 8.5 x the diameter of the Earth – and covers roughly 1/3 of the distance from Earth to the moon.

Source: Linden Thomas & Company

Naturally, this staggering amount of money would be difficult to fit inside your house, let alone your wallet! But it does make one wonder: just how much could someone buy with a trillion dollars? To translate these numbers into something relatable, we did the math to figure out how much a trillion would buy of a wide range of items.

Consider the following. One trillion dollars would buy you approximately:

- 456 billion McDonald’s hamburgers (70x the current production of MacDonald’s globally), or

- 20 million new cars (e.g. BMW 330i) (25% more than the entire US auto industry produces each year).

- 1 billion acres of land in Africa (roughly 55% of the entire continent).

- 77 Ford-class aircraft carriers (for comparison, the US navy has 11 aircraft carriers, China has only 3 and it declines from there.)

Source: Linden Thomas & Company

But this is the point where we have to urge caution. It’s easy to get caught up in speculation about what you might buy if you were that wealthy. Too easy, in fact. The market’s fawning over successful IPO’s (thus far, at least) can be so enticing that otherwise intelligent people can be drawn in to the euphoria and abandon sound principles.

Both Wall Street and the media have mutual interest in amplifying these stories. And once the hype machine cranks up, it can be like a siren song to unsuspecting investors. For instance, Goldman Sachs analysts publicly projected SpaceX revenues climbing 100-fold by 2030. Not to be outdone, Morgan Stanley analysts published research claiming SpaceX annual revenues would reach $3.4 trillion by 2040. In the case of JP Morgan, famed CEO Jamie Dimon himself hosted a sales pitch for SpaceX at its Park Avenue headquarters calling SpaceX a once-in-a-generation opportunity.

With respect to the news media, this story went way beyond the traditional financial news media (e.g. Wall Street Journal and Bloomberg) and was carried by a wide range of mainstream media companies (e.g. CNN, NY Times, ABC news, etc.). For instance, the New York Times ushered in stories of orbital data centers, asteroid mining, and lunar hotels. CNBC reported breathlessly on the ‘fever pitch’ driving massive interest in the name. While Reuters featured a human interest story on Musk becoming the world’s first trillionaire.

No doubt, SpaceX is an engineering marvel. They are the first company to engineer reusable rockets – which radically alters the economics of going to space. Before SpaceX, it cost roughly $10,000 to $18,500 per kilogram to launch a satellite. Since SpaceX developed orbital class reusable rockets (Falcon), the cost per kilogram has declined all the way down to $2,700 to $3,500, roughly a -72% to -81% decline in launch costs. A true game changer.

Source: Linden Thomas & Company

However, the capital costs are still enormous. And charting new territory is always fraught with risks. The company has already spent more than $15 billion on just the Starship program in CAPX in 2026 YTD; and they have made more than $25 billion in commitments for AI /compute infrastructure for 2026-2027, among many other things. Wall Street expects this $75 billion capital raise to last the company only 2-3 years. Moreover, all this spending makes the company’s financial statements heavily front-loaded as they build their infrastructure. In fact, they still haven’t turned a profit. In the company’s recently published S-1 filing, the company reported a loss from operations in 2025 of -$2.6 billion. And that means despite the successful IPO, the company is still relying on the generosity of strangers to keep the business afloat. And all that needs to happen is for these strangers to have a change of heart – for any reason, good or bad – and the company could face a crisis.

As any student of market history knows, market sentiment can shift wildly. For instance, in early 2000, there was still enough euphoria during the Tech Bubble to fund the AOL/Time Warner mega deal. But by the end of that year, funding for the tech space had completely dried up and all tech companies were crashing -including the good ones that are around today. In the collapse of the Tech Bubble, the NASDAQ declined -83% from its peak in March of 2000. We don’t know if that kind of bubble popping is just around the corner. But it sure could be. And today, the writing is on the wall. The major hyperscalers are sharply competing for the leading position in AI – collectively projected to invest over $1.8 trillion in data centers over the next 4 years. The technology comes with massive promise. No one doubts that. But the timing and calibration of the revenues with the inherent economics of the business are yet to be discovered.

Moreover, Wall Street gets paid (handsomely) by bringing companies public. Typically, the investment banks earn roughly 5-7% of the proceeds raised in an IPO. Technically, they buy the shares offered in the raise at a discount, and then turn around and sell them at a higher price, earning a spread. So, their interests are generally very narrow – to buy and unload all of the shares in an IPO as quickly and orderly as possible.

In the case of a giant IPO like SpaceX, the banks earned only 0.7%. But based on the $75 billion raise, the fees were still enormous at roughly $500 million on one deal. (The two lead underwriters on the SpaceX IPO, Goldman Sachs and Morgan Stanley each took home $100 million.) Thus, the investment banks have a huge incentive to sell the deal, but not to earn money for you, the investor. Bringing companies public and managing investments for your long-term wealth are two vastly different worlds. To appreciate the magnitude of these incentives, consider the fees earned by the investment banking syndicate for just the SpaceX IPO:

Source: Linden Thomas & Company

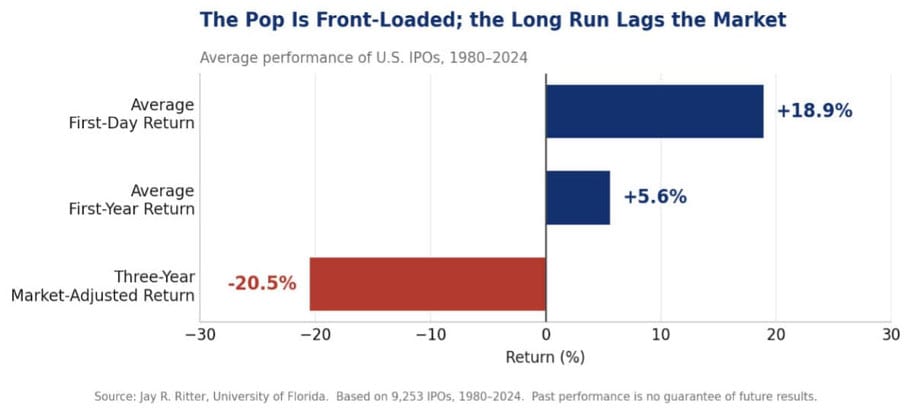

However, savvy investors know that the IPO market tends to fare well in the very short term (measured in days after IPO), but then can roll over and perform poorly in the months and years after the IPO date. The following table shows the performance of all IPO’s over the past 45 years (since 1980):

As illustrated in the table, IPO’s tend to underperform the market dramatically in the three years post IPO. How this comes about is that investment banks pick and choose which companies to bring public by staying acutely aware of what they can sell to the public at moments in time. They simply sell what they can when they can. But wise investors know that Wall Street is often selling a mirage. Very few IPO companies, if any, go up and up on a straight line and never experience the setbacks, losses, drawdowns, recessions, competition, credit crises, etc. that define the real world. And this includes great companies that are true innovators, like SpaceX.

So, as an investor, it’s appropriate to be excited about the innovative things SpaceX is doing. But your enthusiasm must be tempered by the knowledge that the economics of the business have yet to be fully established. And chasing returns now due to the current excitement about SpaceX would be a violation of the hard-earned principles of wisdom in investing: Stick to a sound plan. Stay invested through good times and bad. And spread risk.